October 2023 monthly investment news

September saw equity markets retreat from their recent highs as bond yields rose and central banks maintained somewhat of a hawkish stance, writes Richard Temperley.

With the rally in risk assets seen throughout the year, September served as a cautious ‘step back’ for investor sentiment. Economic data suggested a slowdown in many regions as the effect of higher interest rates filters through to economic activity. Despite this, the US labour market remains strong albeit with some indicators such as unemployment rising in September. The area of job growth continues to be a focus in the US, as inflationary pressures are largely dependent on wage costs. Energy prices rose throughout the month, in contrast to their downward trend over much of 2023.

Activity

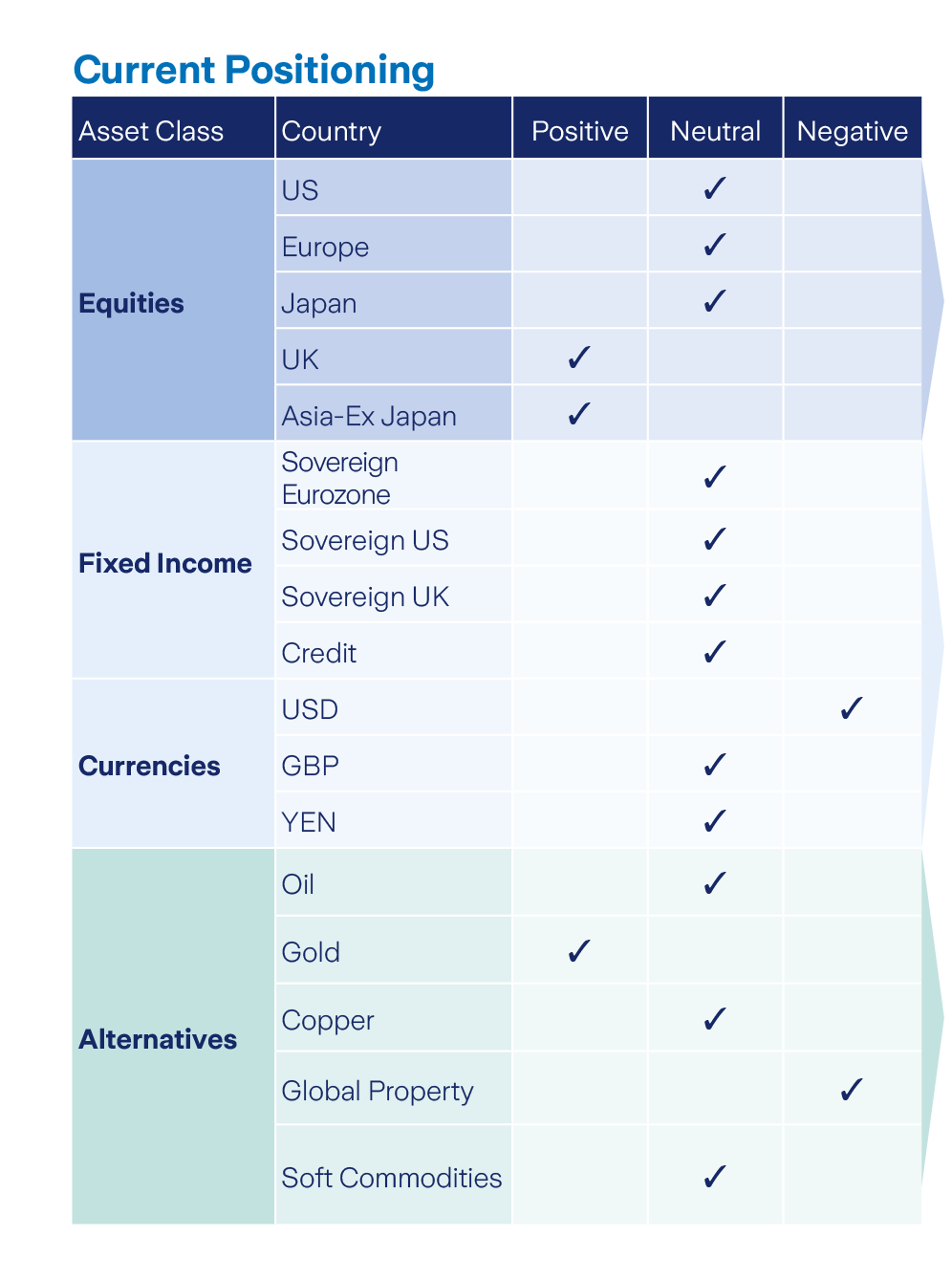

Throughout the month of September, our positioning was overweight equities and long duration bonds. We maintained our overweight position in equities despite the recent dip in performance for risk assets. We have also maintained our long duration bond position as we believe higher rates are a short-term concern. Based on current market conditions, there may be an opportunity to add to bond positions from this point. This may lead to our first positive sovereign bond positioning in the past several years. Our Euro Dollar hedge remains in place for some US exposures.

Equity markets

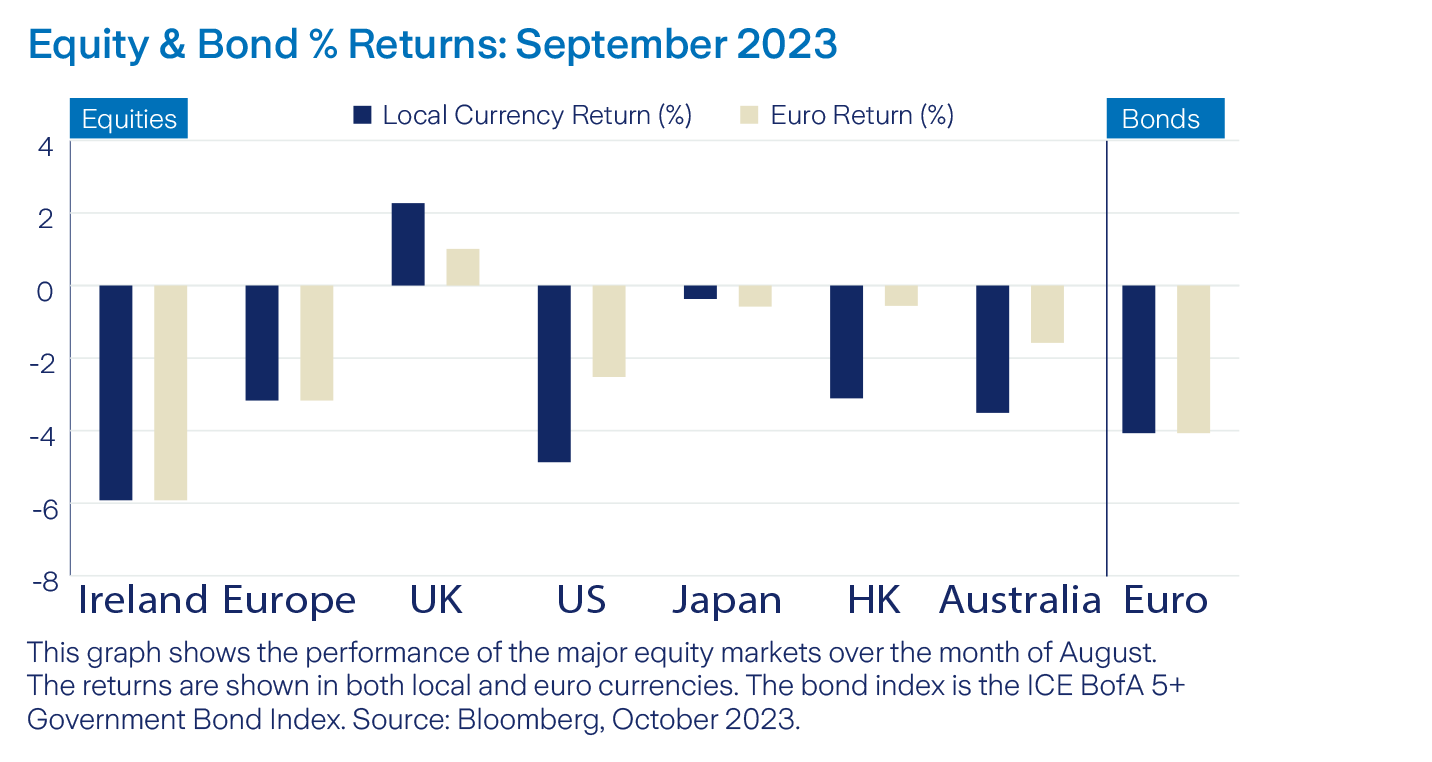

World equities were down -1.9% in Euro terms throughout the month of September. Many of the outperforming sectors year to date reversed some of their gains in September with only the Energy and Finance sectors showing positive returns over the month. The worst performing global sector in September was Information Technology, returning -4.5%. However, year to date this sector has returned 32.3%. In Euro terms the only major market to have a positive month was UK equities, up 1.0%. Much of this came due to surprise economic growth in the UK, which showed that the UK economy fared better than expected in the second quarter of 2023.

Bonds and interest rates

September saw bond yields continue to rise as investors revaluated their position on future interest rates. In the US, the Federal Open Market Committee’s September meeting saw the Fed’s forecasted interest rate increase. Although largely driven by interest expectations, recession risk and slowing economic growth concerns in Europe dragged yields down. Eurozone sovereign bond yields increased sharply towards the end of September on the back of news of an Italian budget deficit. Similarly, higher oil prices throughout the month fuelled worries of sustained inflation. The benchmark ICE BofA 5+ Year Euro Government bond index was down -4.1% in September.

Commodities and currencies

Crude oil prices rose throughout the month of September as a result of ongoing supply constraints with the benchmark West Texas Intermediate Crude oil rising 9.8% throughout the month. Despite lower prices in the first half of the year, crude oil has continued on an upward trend since June. Precious metals such as gold traded under downward pressure as bond yields rose throughout the month of September. Gold was down -1.3% in euro terms for the month. The US dollar strengthened against a basket of currencies in September as economic indicators suggested a robust US economy. At the end of the month 1 Euro purchased 1.0573 US Dollars.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these products you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()