September 2023 monthly investment news

August saw risk assets retreat as sentiment declined off recent highs with markets trimming the previous gains equities had experienced throughout much of 2023, writes Richard Temperley.

A large driver of this sentiment was slowing growth indicators and interest rate expectations. In the US, a higher headline inflation prints, and somewhat hawkish Federal Reserve meeting saw investors reprice the possibility of further rate hikes. August also saw the annual Jackson Hole Economic Symposium take place, famous for its Fed chairman speeches which tend to function as an outlook for future monetary policy. Chairman Jerome Powell’s speech was generally well received by markets, in contrast to last years which sent markets significantly lower. Some commentators however did note a hawkish tone regarding the potential for a further rate hike.

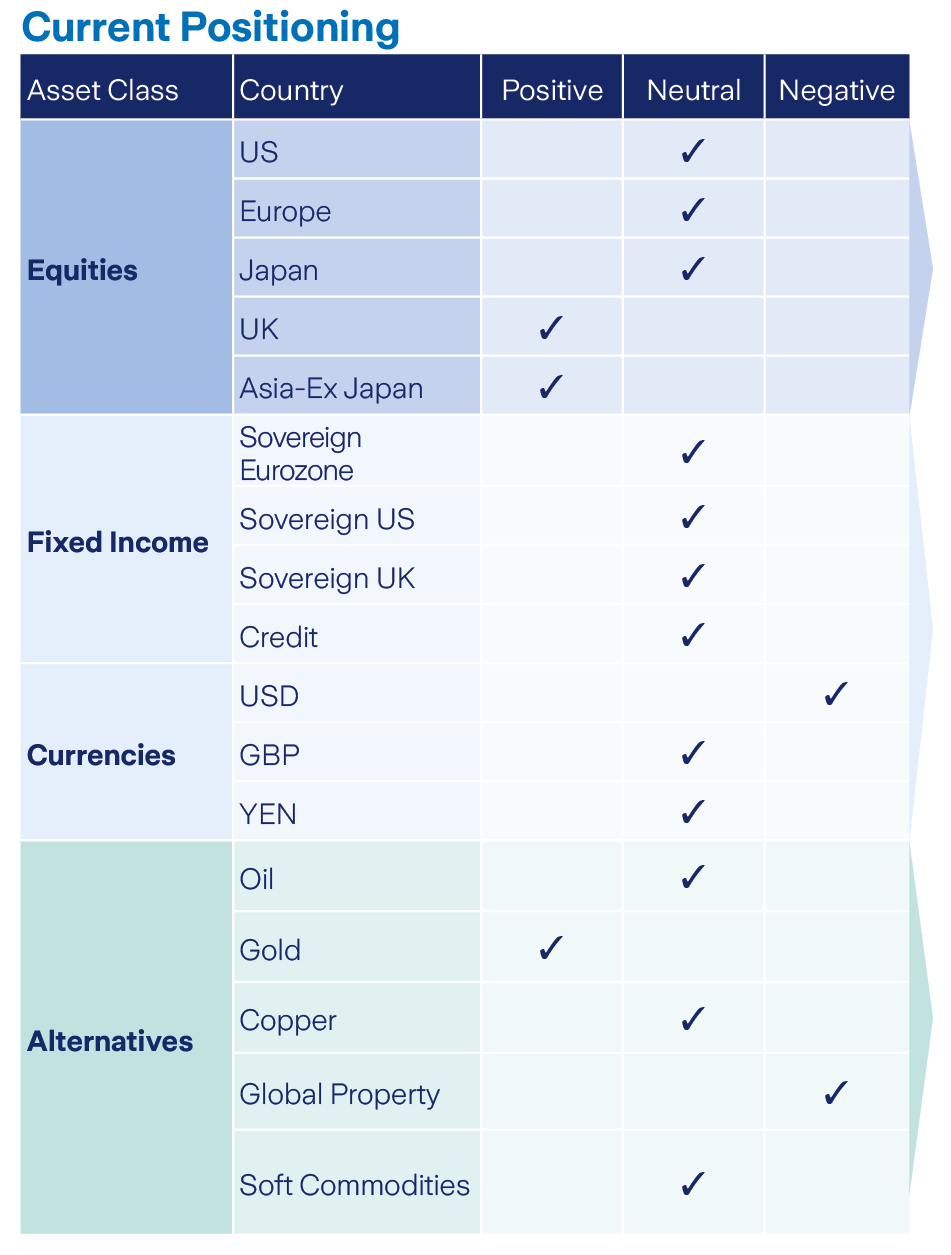

Activity

Throughout August our preference for equities was maintained, however we remain flexible in this position as equities come off recent highs.

Within our equity allocation we favour companies in technology, materials, and energy sectors. This preference has been beneficial to our relative performance through August, as such our equity allocation is positioned to favour a slight growth bias.

2023 has seen better value in bonds and we have lengthened the duration of our fixed income allocation throughout the year. Interest rate concerns remain the predominant theme in markets however strong earnings have helped support valuations. Our Euro Dollar hedge remains in place.

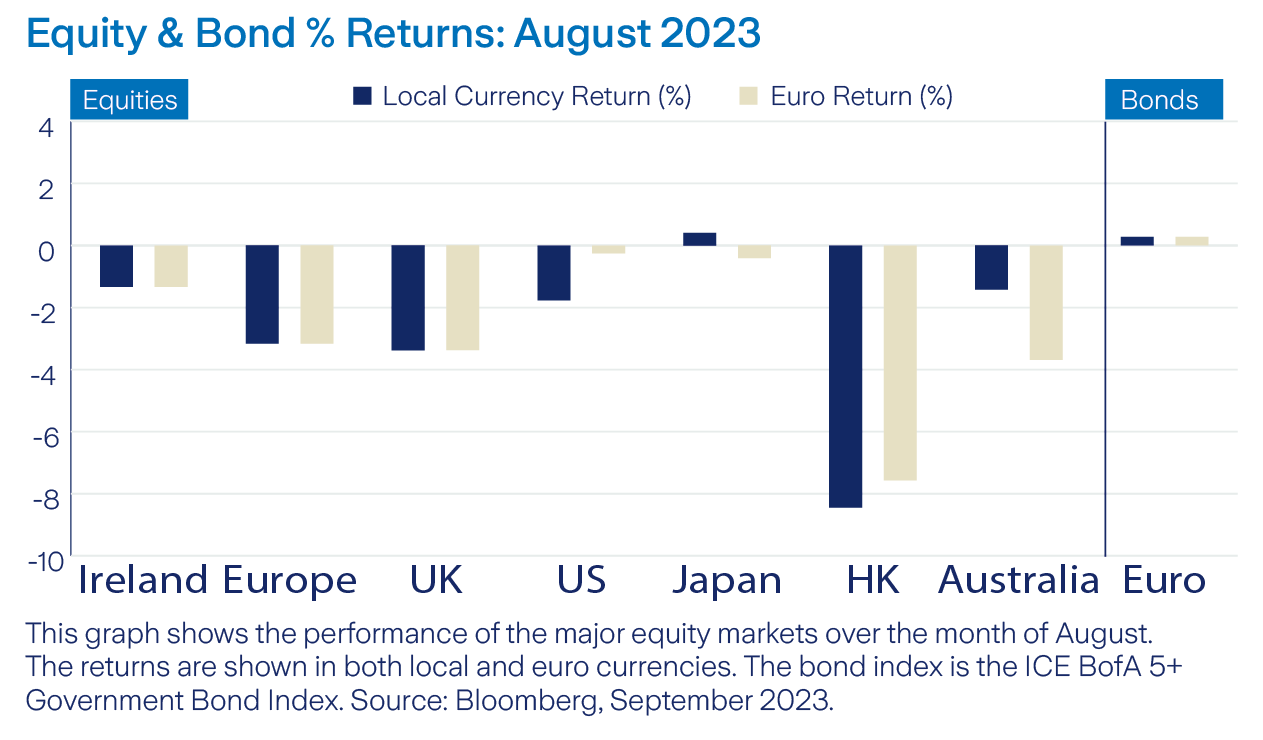

Market performance

Equity markets

The month of August saw equities retreat from strong gains seen throughout much of the year. A traditionally quieter month for trading volumes, August saw muted activity for equities with many investors holding back from taking concentrated positions.

On a global sector basis, energy stocks were the clear outperformer returning 3.5% in euro terms. The sector has been volatile throughout 2023, posting several negative months. The worst performing sector globally in August was Utilities, down -3.90% in euro terms.

Year-to-date, utilities are also negative (-4.17%), despite most equities posting gains throughout the year, highlighting the bias of growth performance in 2023.

Bonds and interest rates

August saw global bond markets remain volatile with upward pressure on yields hurting some investor returns in fixed income. At the beginning of August credit rating agency Fitch downgraded the US governments credit rating from AAA to AA+ citing fiscal concerns.

Yields on eurozone government bonds rose initially in August but tapered off slightly as sentiment improved, the benchmark 10-year German Bund yield finished the month slightly lower at 2.462%, down from 2.489% the previous month. Despite volatility, bonds finished the month up, with the ICE BofA 5+ Year Euro Government index returning 0.3%.

Commodities and currencies

Oil prices rose in September, with the benchmark West Texas Intermediate Crude Oil up 4.5% in euro terms. Much of the rise in energy related commodities came as a result of Saudi Arabian oil production cuts. OPEC+, a group of countries which control over half the worlds oil production, hinted at potentially increasing supply cuts for the remainder of 2023.

Despite the gains seen in oil, both precious metals and base metals saw a decrease in price over the month as macroeconomic data suggested a slower growth outlook globally. Copper, often used as a barometer for global economic health, was down –3.6% in euro terms.

US Dollar strength increased against the Euro throughout August as risk appetite declined. At the end of the month, one dollar purchased 1.0843 Euros.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these products you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()