November 2025 monthly investment news

October’s investment markets were shaped by political uncertainty and cautious central bank policies. Get the full insight in this month’s market news.

The US government shutdown led to a gap in economic data releases, adding complexity for investors and policymakers. Central banks weighed inflation trends against ongoing geopolitical and trade uncertainties, with the Federal Reserve adjusting rates in response to softer inflation, while the European Central Bank held rates steady.

Equity markets saw early volatility from US–China trade tensions, but sentiment improved with positive trade developments and strong corporate earnings. Commodities were mixed, as gold prices rose on central bank demand and oil prices fell. Meanwhile, the euro weakened against the US dollar, reflecting diverging economic and policy outlooks across regions.

Market activity

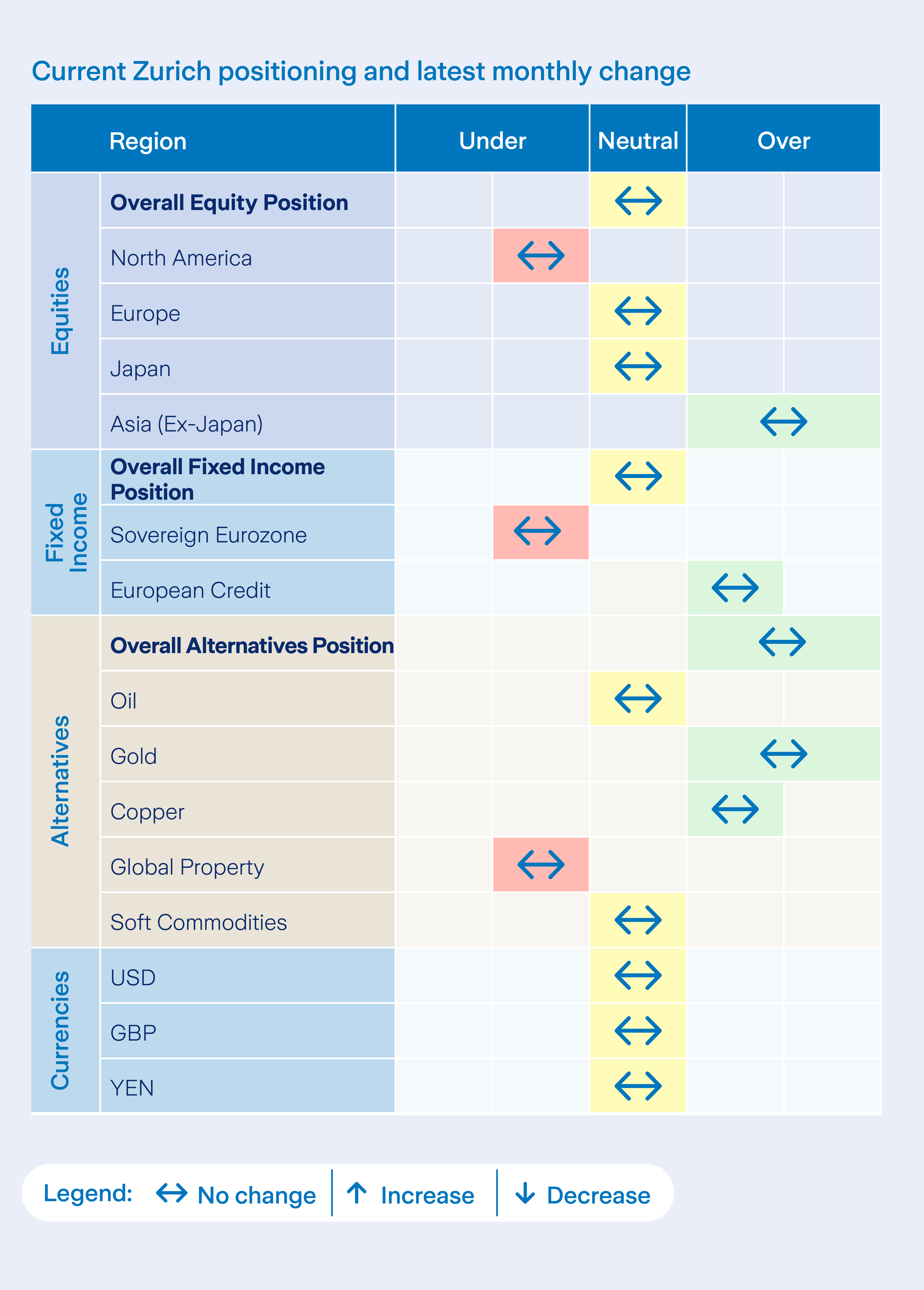

In October, we increased our allocation to the new real estate-focused fund, with additions made in two tranches. This now serves as the global property component in our Active Asset Allocation (AAA) and multi-asset funds. This fund tracks major real estate companies in developed markets. These were the only significant active allocation decisions for the month.

Currently, we are close to neutral in equities within multi-asset funds, favouring Asia Pacific over US stocks. In fixed income, we prefer shorter duration and have a slight tilt towards short-term credit over sovereign bonds. Our portfolio also maintains an overweight position in gold.

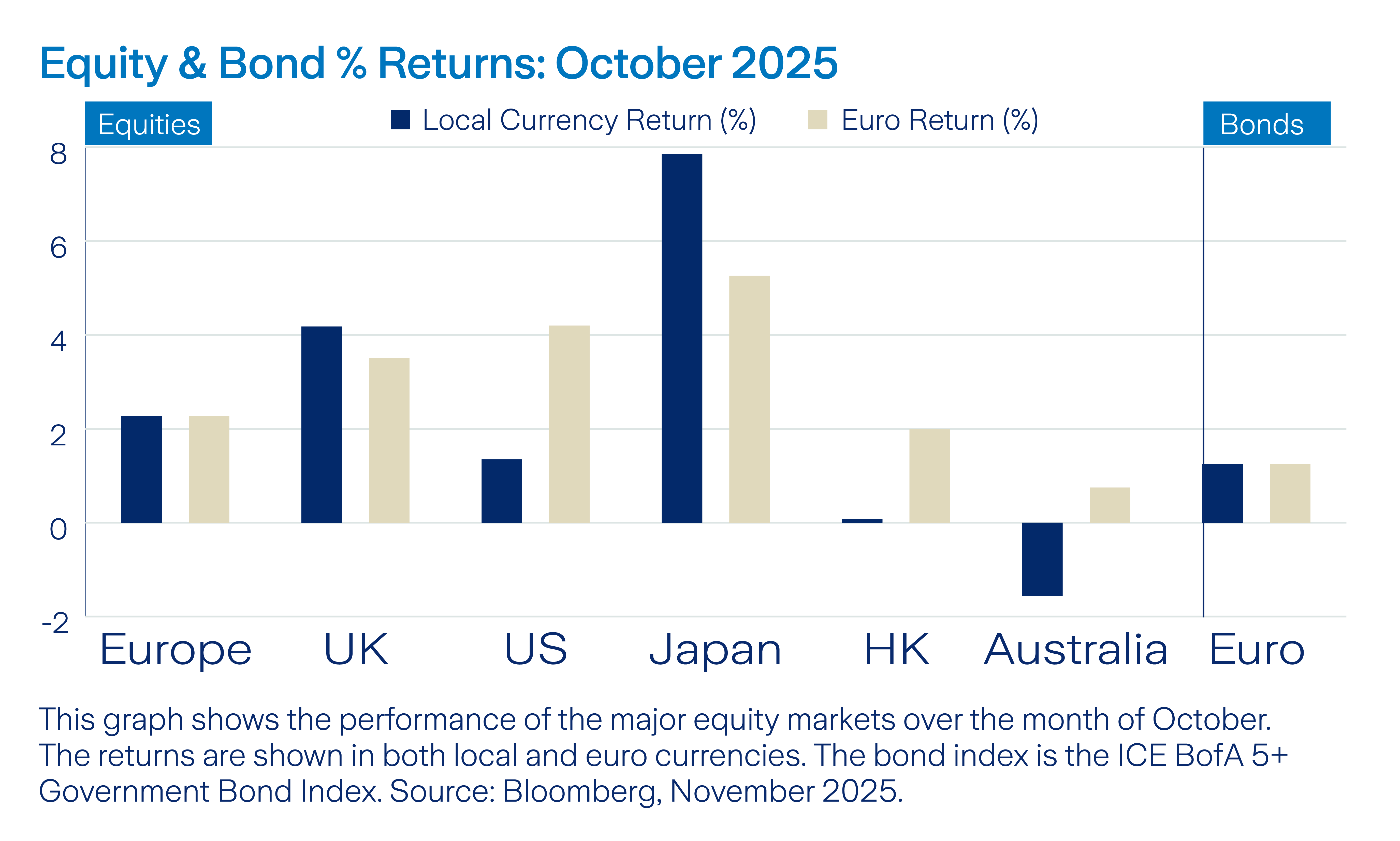

Equity markets

Global equities delivered positive returns in October. Markets saw early declines due to renewed US–China trade tensions over rare earth mineral export controls, a key element in the artificial intelligence (AI) supply chain.

Sentiment improved following a temporary trade agreement that eased tariffs and restrictions. Strong third-quarter earnings also supported market performance, with the majority of reporting companies exceeding expectations.

By month-end, most MSCI sectors posted gains, led by Information Technology and Health Care, which returned 8.3% and 4.9% respectively. Materials and Real Estate were the worst performers for the month, returning -1.1% and -0.8% in euro terms.

Bonds and interest rates

Softer inflation in October gave the Federal Reserve the confidence to implement a 25-basis point rate cut, bringing its target range down to 3.75–4.00%. However, Jerome Powell indicated that additional cuts in December were uncertain.

Global government bond markets generally saw positive returns, as yields declined across major regions thanks to supportive central bank actions. Still, the US government shutdown and ongoing tariff concerns tempered risk appetite.

The 10-year US Treasury yield reached a low of 3.95% before ending at 4.08%. The European Central Bank held its rate steady at 2%, confident in the eurozone’s resilience and easing inflation.

Commodities and currencies

Gold rose 3.7% in USD terms in October, supported by heightened concerns over slowing global growth, which boosted demand for safe-haven assets. Early in the month, gold exceeded $4,000 per ounce for the first time.

Currency markets saw the euro weaken against the US dollar, ending the period at 1.154, down from 1.173 in September.

Oil prices fell to their lowest levels since 2021, with WTI ending the month at $60.98 per barrel, pressured by oversupply concerns and increased inventories.

OPEC+ maintained only a modest output increase, but easing geopolitical tensions contributed to weaker prices.

Warning: Annual management fees apply. The fund growth shown below is before the full annual management charge is applied on your policy.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: Past performance is not a reliable guide to future performance.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these products you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()