October 2025 monthly investment news

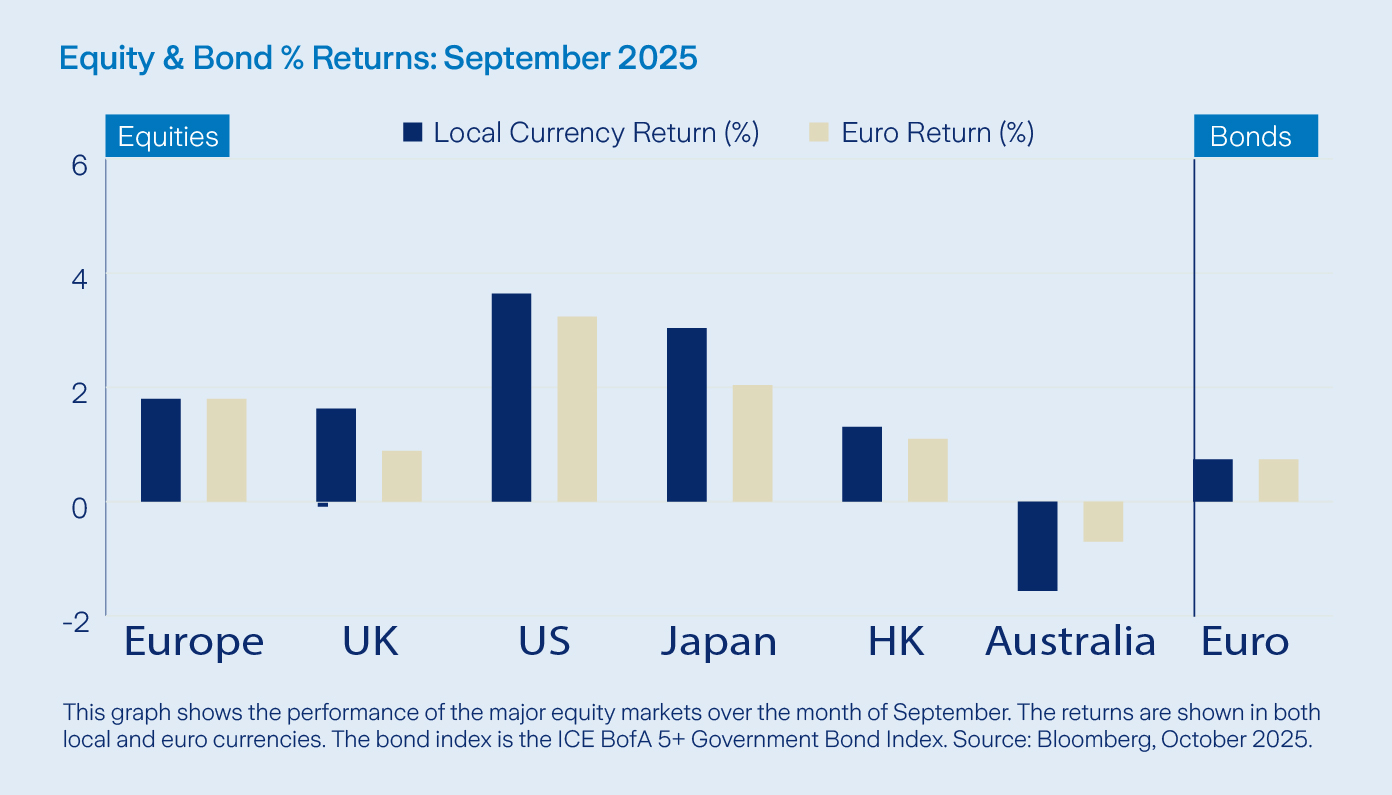

US equities continued their upward trend in September, driven by optimism in technology, shifts in monetary policy, and positive labour market developments.

Global stock markets advanced last month, although the pace slowed in developed regions. However, favourable currency movements, attractive valuations, and supportive policies offered some momentum.

The FOMC cut the Fed Funds Rate by 25 basis points, the first reduction since December 2024, providing a boost to fixed income markets. Commodities delivered positive returns overall, despite mixed performance among individual components.

Precious metals stood out, with gold prices soaring to reach new highs. Factors such as renewed inflation concerns, the Fed’s rate cut, and worries about the US government shutdown helped drive demand for the safe haven asset.

Market activity

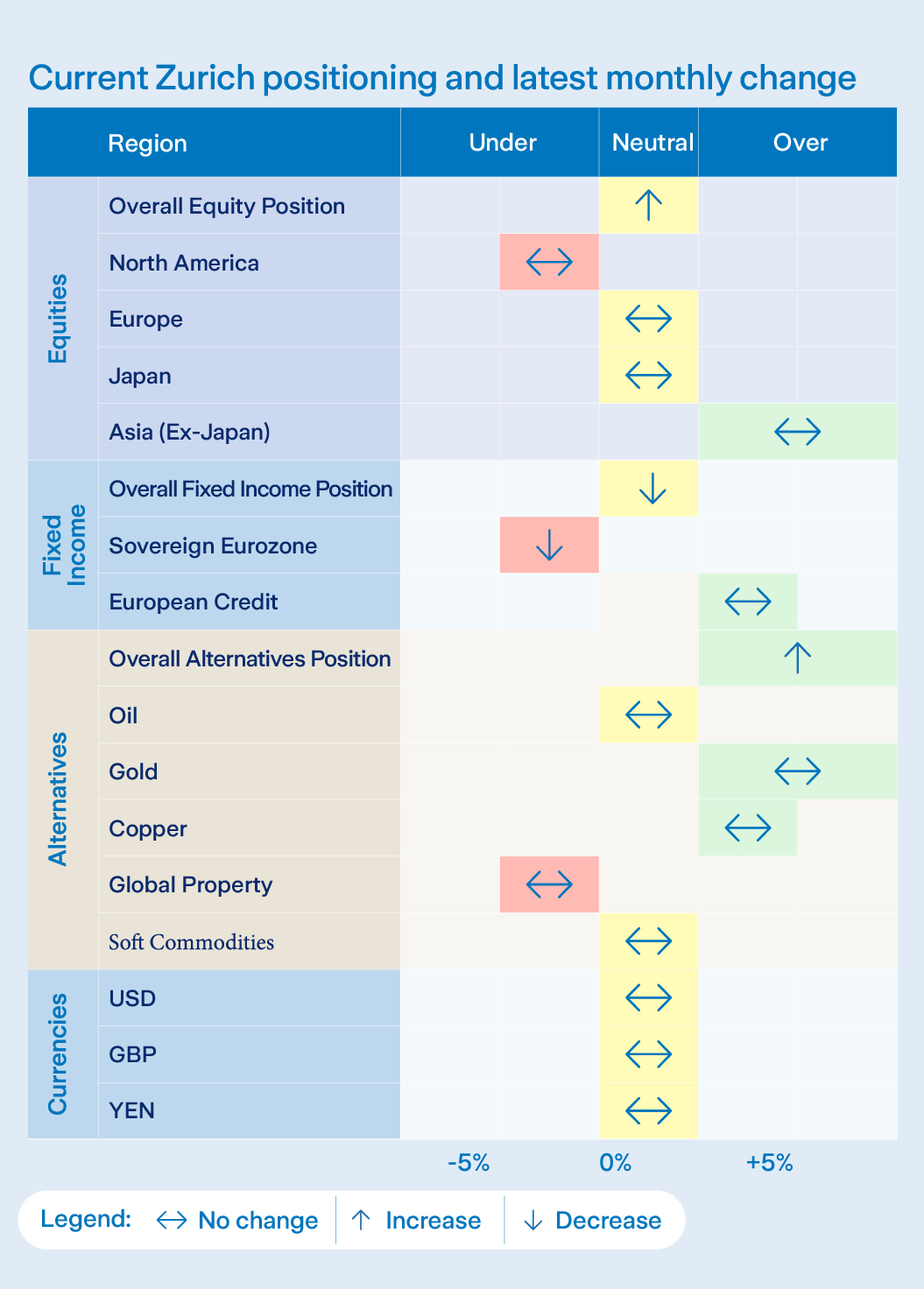

In September, we incorporated a new real estate-focused allocation, now serving as the global property component within the Active Asset Allocation (AAA) fund and multi-asset funds. This fund tracks an index of the largest real estate companies in developed equity markets. From a sector perspective, we favour Communication Services, Materials and Industrials while remaining underweight in Consumer Staples, Energy and Utilities. We also have an overweight position in gold and a slightly short bond duration. Regionally, our equity allocation remains underweight in the US, overweight in Asia Pacific, and broadly neutral across Europe and Japan.

Equity markets

Major US equity indices closed September on a positive note, propelled by ongoing momentum in AI-driven stocks, strong corporate earnings, and renewed optimism following an interest rate cut.

European equities also advanced, supported by encouraging economic data and strong earnings, though France saw a decline due to concerns about political instability. Chinese equities performed well as government efforts to address price wars and improving industrial profits provided support.

Globally, Information Technology (+7.0%) and Communication Services (+4.3%) led sector performance, while Consumer Staples (-2.4%) and Energy (-0.8%) lagged, reflecting investors’ focus on a handful of mega-cap stocks.

Bonds and interest rates

In September, the Federal Reserve lowered the federal funds rate by 25 basis points to a range of 4%–4.25%, marking its first cut since December 2024. Chair Jerome Powell described this as a “middle path”, seeking to balance ongoing inflation pressures with signs of a softening labour market. Meanwhile, the ECB maintained its deposit rate at 2%.

President Christine Lagarde emphasised patience and pointed to risks from the ongoing US–EU tariff dispute. US 10-year Treasury yields dipped to 4.02% mid-month, then rose up to 4.15%.

Eurozone bond markets remained steady, with 10-year German bund yields holding close to 2.7%.

Commodities and currencies

WTI oil prices dropped to $62.37 per barrel in September, as concerns over abundant supply and weakening demand outweighed hopes that the Federal Reserve’s first rate cut of the year would spur greater consumption.

Gold gained by 11.9% in USD terms, driven by economic uncertainty and expectations of further Fed rate cuts, prompting investors to seek safety.

The US dollar lost ground against the Euro, with 1 Euro purchasing 1.173 USD by month-end, up from 1.169 at August’s close. Softer US economic data and worries about a widening budget deficit reduced global demand for the dollar.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: If you invest in these products you may lose some or all of the money you invest.

Warning: The value of your investment may go down as well as up.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()