Why investment returns matter for your employees’ final pension pot

At Zurich, we believe consistent investment performance is at the heart of delivering real value to pension scheme members. Alongside effective member engagement and robust governance, it is strong returns that can help secure a brighter financial future for employees, writes Eadaoin Murphy, Investment Solutions Analyst.

Increasingly, employees rely on their employer for guidance and support in planning for their long-term financial wellbeing. That’s why the investment strategy behind your company pension plan is so important - it’s the engine driving the growth of employees’ retirement savings.

As an employer, the choices you make about default investment design, contribution structures, and communications can meaningfully improve employees’ retirement outcomes. Here’s why investment returns matter - and what you can do about it.

In a Defined Contribution or Master Trust scheme, employees’ future income depends on both contributions made and the returns achieved by the scheme’s investments. Most employees rely on the scheme’s default investment strategy, making its performance a critical factor in achieving their retirement goals. Put simply: over time, returns do more of the heavy lifting than contributions alone.

Employers should consider the following when assessing investment performance:

Is your scheme delivering strong, consistent returns?

Investment performance is the primary driver of pension adequacy. Is your fund meeting expectations, especially during growth phases? Reviewing how your investment manager performs through different market cycles can reveal whether real value is being added for your employees.

How does your default investment strategy compare to its peers?

Benchmarking your scheme’s performance against others can help identify strengths and opportunities for improvement, ensuring your employees benefit from competitive returns.

Are members engaged with their investments?

Supporting employees to understand how their savings are invested empowers them to make informed decisions, further enhancing the potential for positive retirement outcomes. Each quarter Zurich creates a bespoke magazine for employees of pension schemes called “Pension Matters”, if you are not already sharing this with your employees it’s not too late to start!

Does your investment approach integrate ESG (environmental, social, and governance) principles?

Today, both employers and employees value responsible investment. Ensuring your scheme is aligned with your organisation’s sustainability goals can drive both better financial and societal outcomes.

Does your scheme offer flexibility and a proven process?

A strong track record of out-performance, supported by a robust, consistent investment process, gives employees greater confidence in their pension journey.

Zurich’s track record of out-performance

Zurich has been recognised by Brokers Ireland as number one for investment excellence since 2014 and was fund management company of the year 2025 at the Business and Finance FS Awards. Our funds are managed using Zurich Investments’ active, top-down process - delivering consistent out-performance within well-defined risk parameters.

- Prisma 5, our core fund for Defined Contribution growth, achieved outstanding annualised five-year returns of 10.5%. (Nov 2025) *

- Our flagship Balanced Fund delivered an annualised return of 8.1% over the past 30 years. (Nov 2025) *

These strong results mean that employees retiring with Zurich have enjoyed greater financial security, thanks to better investment returns.

The journey to retirement

Members of the Zurich Master Trust are automatically placed in the default investment strategy. This default is a ‘lifestyle’ investment strategy, which means the pension fund is invested to match the members pension fund journey.

In the early years, savings are mainly invested in higher-risk assets, like shares (equities), which offer more growth potential but can fluctuate in value. When approaching retirement, investments are gradually shifted to destination funds based on your personalised benefit mix. These funds may include bonds or cash, which are generally more stable but may have lower returns.

The aim is to help the pension fund grow when a member is younger and can take more risk, and then reduce their risk exposure as they near retirement, shifting into funds based on their personalised benefit mix.

The Zurich Master Trust uses Zurich’s Personalised GuidePath (PGP) strategy as the default investment approach. The standard setting when a member joins the Scheme is:

Medium Risk/Return growth stage

Retirement planning stage targeting 75% ARF and 25% tax-free cash

Strategy end age matching the employer section’s Normal Retirement Age (NRA)

A member can personalise GuidePath at any time through their online dashboard. The dashboard allows them to increase or decrease the risk/return level. Additionally, they can select different target retirement benefits or target a different retirement age.

The employer’s role in better outcomes

Most employees will stick with the default investment option their employer provides. That’s why it’s crucial to design a default fund that is well-diversified, cost-effective, and suited to the needs of your workforce. Reviewing your default fund regularly, and adjusting, when necessary, is the single most powerful step you can take to improve outcomes for many of your members.

Clear and accessible communication

Clear, jargon-free communication is essential. By providing information in everyday language, you can help employees understand their options and encourage them to take positive actions, whether that’s adjusting contributions, thinking about their appetite for risk, or exploring retirement choices at key points in their careers. Simple, timely communications make it easier for people to engage when it matters most.

Navigating market volatility

Market ups and downs are a normal part of long-term investing but can be unsettling for employees. Explaining volatility in simple terms, and reassuring members that temporary declines are normal while the long-term focus is on growth, can help employees stay confident and avoid panic-driven decisions.

Leveraging career milestones

Major career moments are perfect opportunities to help employees review their retirement plans. Encourage members to check in on their investments and contributions when they join, receive a promotion, reach the halfway point to retirement, or are within a few years of retiring. These milestones make it easier for employees to focus on their goals and make informed decisions.

Supporting goal setting

Support employees in setting concrete objectives, such as aiming to replace a certain percentage of their salary in retirement. Offering practical tools or sessions to help set and monitor these goals gives employees more confidence in their progress and helps them stay on track for the future they want.

Expert support from Zurich

Call on the support of Zurich to help your employees understand and value their pension benefits. Our expert team makes it easy to review and enhance your employee benefits, saving you time and effort while supporting your business goals.

Why Zurich?

Companies are choosing the Zurich Master Trust to avail of our many decades of experience in the Irish market. Zurich has been helping employers and trustees in Ireland make the right decisions about their employees’ futures for over 40 years – we have experts across all strands from trusteeship to investment management through to onboarding and administration, contribution collection and payment of benefits. Employers who choose the Zurich Master Trust can rest assured that their employee benefits are in the best hands. Visit zurichcorporate.ie to find out more.

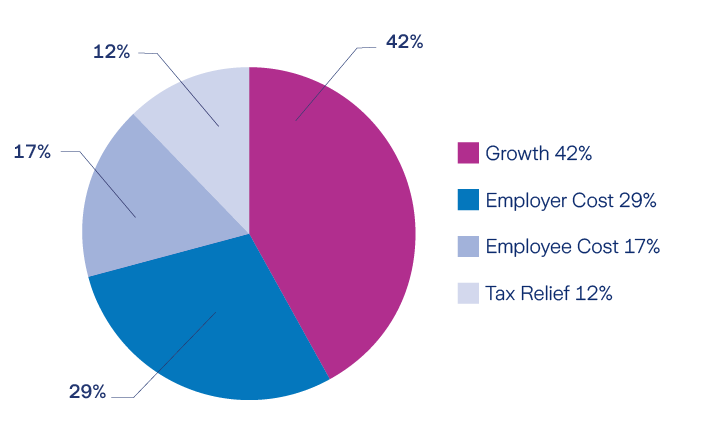

Case study: Employee, age 40, single, salary of €75,000

Factors contributing to pension pot value

| Assumptions | |

| Salary | €75,000 |

| Employer contribution | 5% |

| Employee contribution | 5% |

| Employee tax relief | 40% |

| Term | 26 years |

| Growth after changes | 4% |

Actual investment growth will depend on the performance of the underlying investments and may be more or less than illustrated. Case study includes 100% allocation, 1% Annual Management Charge (AMC) and 4% net growth (5% gross less AMC of 1%).

*Source: Zurich Life November 2025

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these funds you may lose some or all of the money you invest.

Warning: These figures are estimates only. They are not a reliable guide to the future performance of your investment.

Warning: This product may be affected by changes in currency exchange rates.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()