April 2024 monthly investment news

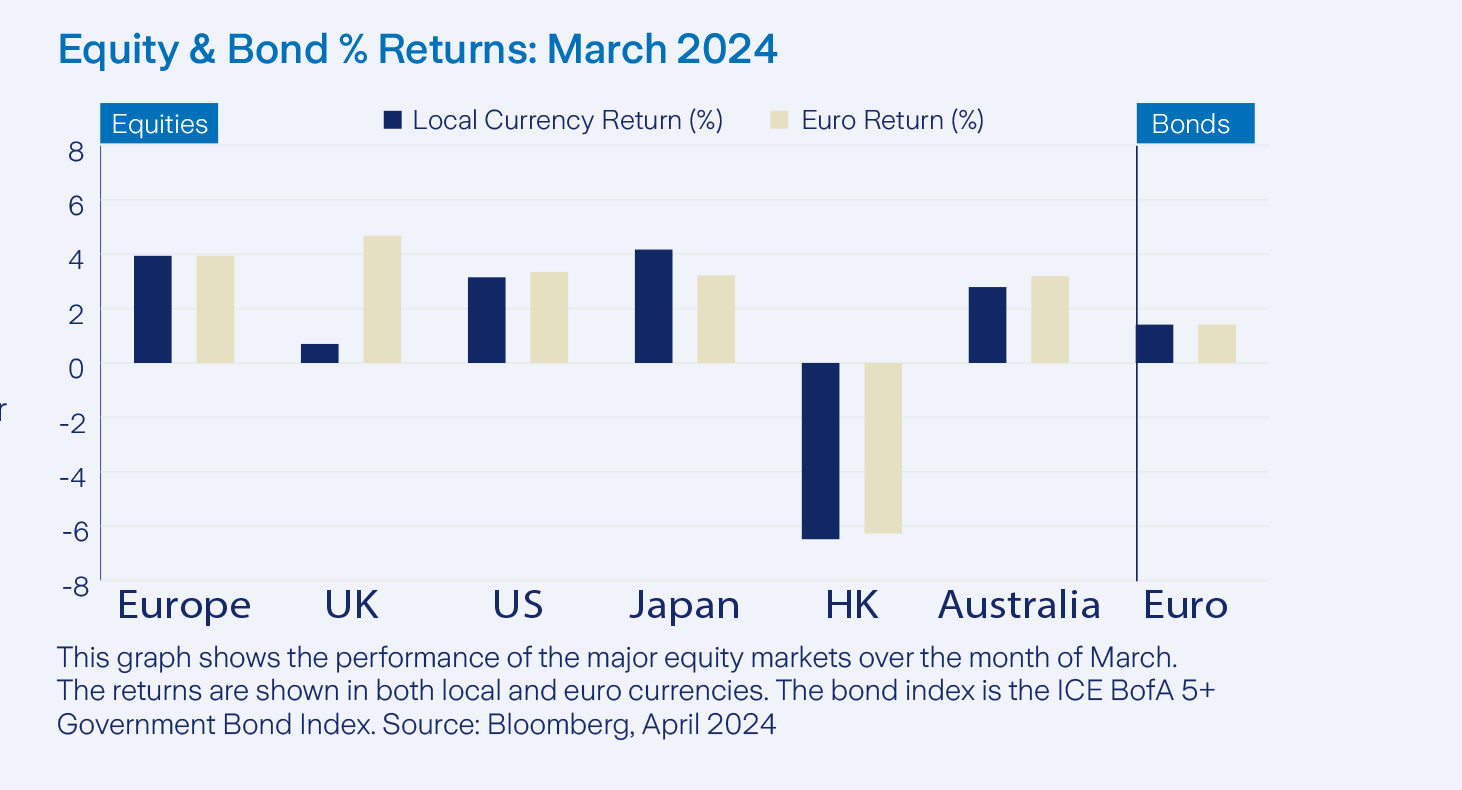

March was another strong month for equities with global stocks up 3.42% for the month in euro terms. This followed a positive February as investors continue to price in the likelihood of future interest rate cuts from global central banks, writes Richard Temperley.

Economic releases in the US indicated that the economy is portraying signs of resilience with improved manufacturing activity. Inflation releases showed mixed results, with some aspects of the US services sector causing headline CPI to inch higher in the US, Core inflation (which strips out the volatile food and energy sectors) ticked lower. In Europe, economic conditions were subdued, with slower manufacturing activity and tight labour markets.

Activity

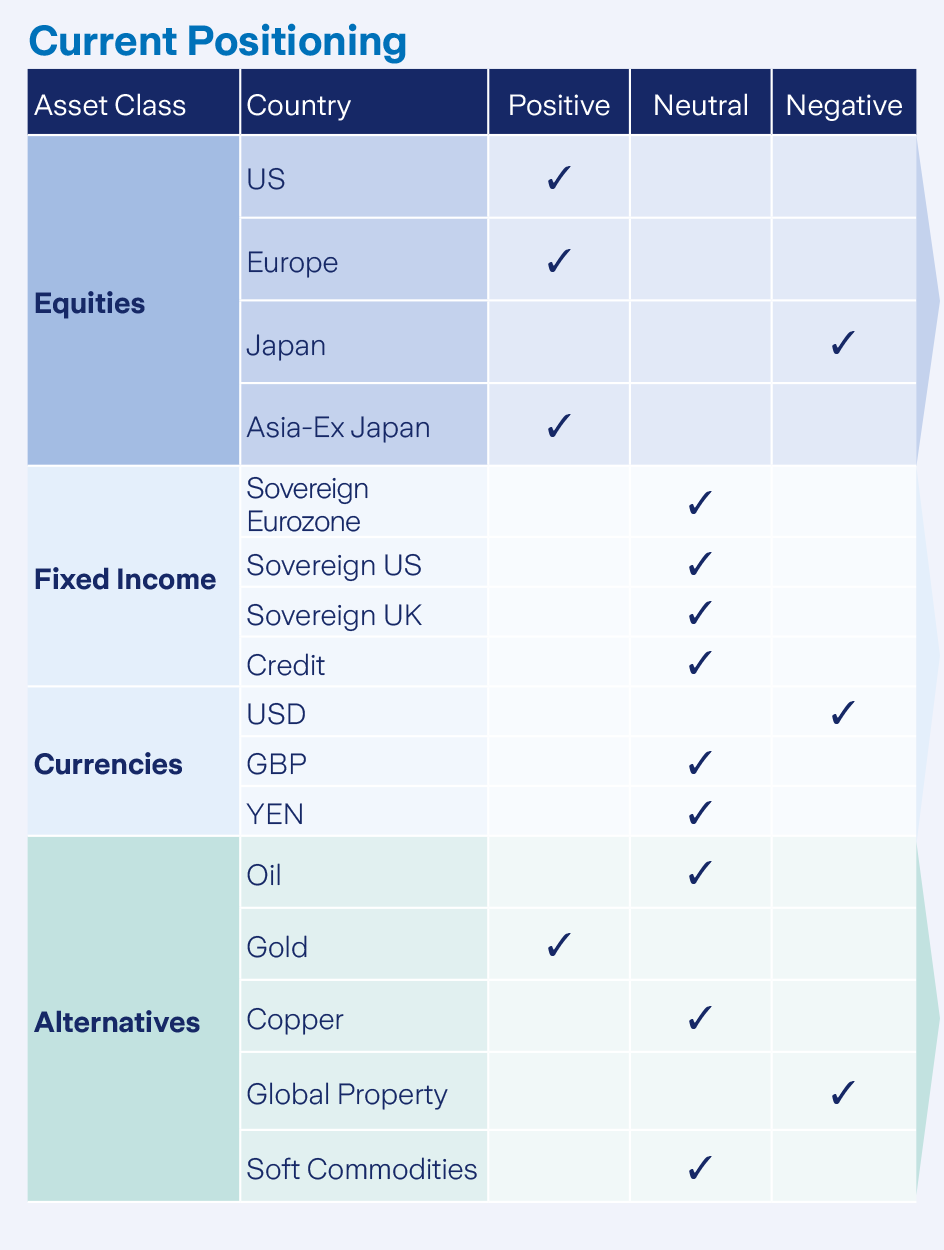

Our current positioning is broadly neutral equities and bonds. Our neutral positioning has allowed for the opportunity to take advantage of recent market performance and pursue opportunities in government bonds and cash, as well as equities. The shift in interest rate environment has allowed for non-equity asset class returns to prove viable and we remain open to further prospects in this area. We favour shorter dated bonds over longer dated government bonds and we await an opportunity to add more longer dated exposures from an asset allocation point of view. Bond markets, as ever, remain a key part of the decision-making process. Our Euro/ Dollar hedge remains in place.

Equity

Markets Equity performance proved strong in March with all major global sectors ending the month in positive territory. Energy was the best performing sector on a global basis, returning 9.28% in euro terms. Much of the sectoral performance was fuelled by higher crude oil prices and a somewhat improved global economic outlook. The worst performing sector globally was consumer discretionary, many of the sector’s major constituents are large cap US stocks which saw underperformance as overall performance in the stock market broadened out, with more companies contributing positively to market performance. The only major market to show negative equity performance in March was Hong Kong, hampered by geopolitical tensions and an economic slowdown in China.

Bonds and interest rates

March was a positive month for bonds as markets priced in the increased likelihood that central banks will cut rates in the summer of 2024. The benchmark 10 Year US Treasury Yield ticked lower ending the month at 4.2%, down from 4.3% the previous month. Inflation in the Eurozone has moved closer to target and several indicators suggested a higher probability of the ECB moving towards an easier monetary policy. In Europe, the spread between sovereign bond yields has narrowed owing to potential rate cuts and the relatively poorer performance of the German economy.

Commodities and currencies

The month of March ended with major commodity prices in positive territory. Gold saw positive inflows as the US Dollar weakened against foreign currencies. The price of the precious metal remained on an upward trajectory throughout the month as weaker economic data indicated a higher probability of future rate cuts. Higher volatility also increased inflows to what is traditionally viewed as a safe haven asset class. Crude Oil prices also increased across the month as geopolitical tensions intensified amidst developments in the middle east. At the end of March 1 Euro purchased 1.079 Dollars.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: If you invest in these products you may lose some or all of the money you invest.

Warning: The value of your investment may go down as well as up.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()