Monthly investment news May 2026

April 2026 demonstrated the resilience of global markets as investors managed persistent geopolitical risks and economic challenges. Read the full report on global investment markets and key fund performance.

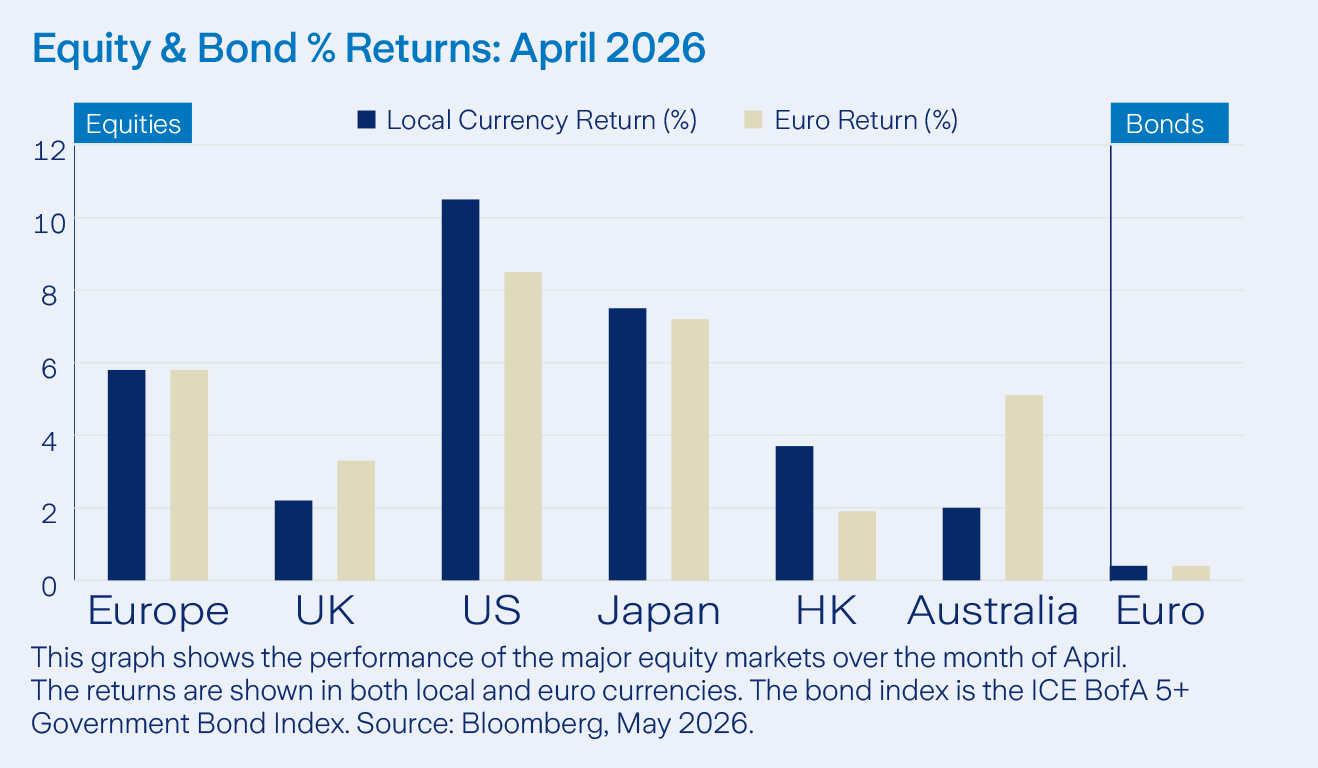

Equities saw solid gains, fuelled by strong corporate earnings and renewed interest in the technology sector, led by artificial intelligence (AI).

Confidence grew as ceasefire discussions between the US and Iran continued, even without a final resolution, which improved investor risk appetite.

Fixed income markets were more volatile in April, government bond yields climbed in response to higher oil prices and ongoing inflation worries. Central banks held interest rates steady but communicated a cautious outlook.

Oil prices surged once again on the back of ongoing supply concerns and geopolitical uncertainties as the Strait of Hormuz remained closed.

Activity

In April, we reduced our broad commodities exposure in the Active Asset Allocation fund (AAA) & Prisma funds, reallocating that portion to oil. This was intended to be a tactical position to benefit from higher oil prices in the near term. There were no other material active asset allocation decisions made in April.

Our current position is modestly underweight equities for the AAA fund. We are overweight in our fixed income allocation for the AAA fund, largely reflecting a preference for short-term bonds over medium or longer maturities, leaving overall bond duration below the benchmark.

Equity markets

Global equity markets delivered solid gains in April, supported by renewed investor confidence in corporate earnings and improving economic stability. Gains were led by large-cap technology and communication companies, as continued enthusiasm for AI drove sector growth.

The earnings season proved healthy, with a majority of firms surpassing expectations. Although energy prices remained elevated due to geopolitical tensions in the Middle East, signs of stabilisation encouraged investors to refocus on corporate fundamentals.

Nine of 11 sectors rose in April in euro terms, led by Technology (15.8%) and communication services (14.7%), while energy (-3.6%) and health care (-1.8%) declined.

Bonds and interest rates

April saw volatility in global bond markets. Expectations for higher interest rates grew due to persistent inflation risks, though central banks remained measured, with both the Federal Reserve and ECB maintaining policy rates but the message from both was one of caution. Hopes for de-escalation in the Middle East lifted government bond prices temporarily following a ceasefire between the US and Iran.

However, by month-end, there was still no resolution, and inflation concerns had resurfaced, pushing yields higher. US 10-year Treasuries touched 4.4%, and Germany’s 10-year Bund yield reached 3.1%.

Commodities and currencies

April’s commodity market remained strong, driven by heightened geopolitical tensions and continued worries over disruptions in oil transit through the Strait of Hormuz. Following a short dip, oil prices climbed again with WTI crude oil ending the month at $105.07 per barrel, up 3.6% in April.

In contrast, precious metals lost ground, with gold and silver returning -2.6% and -3.4% in euro terms. Rising energy prices and changing rate expectations reduced demand for traditional safe havens.

Meanwhile, the US dollar depreciated versus the euro. By month end €1 purchased 1.173 USD from 1.155 at the close of March.

.png)

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these funds you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...