Cash isn't always king

Over the last number of years, returns from investments such as equities and bonds have far exceeded that of cash. That is why we see more investors once again looking at alternatives to holding money on deposit.

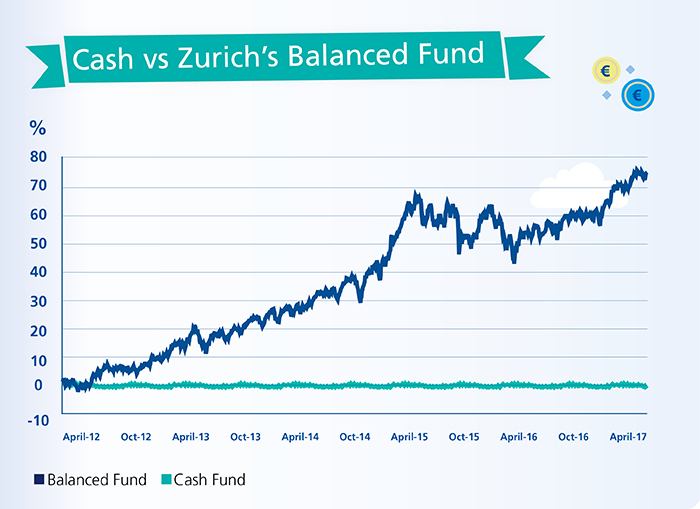

Source: Zurich Life, April 2017. Annual management charges (AMC) apply to figures quoted (30/03/12 to 04/04/17). The fund returns shown are net of the AMC deducted by Zurich Life in our unit prices. The fund returns are based on an investment in the funds and do not represent the returns achieved by individual policies linked to the funds. These fund returns may be before the full AMC is applied to a policy. The actual returns on policies linked to the specified fund will be lower because of the effects of charges and in some cases a higher management charge.

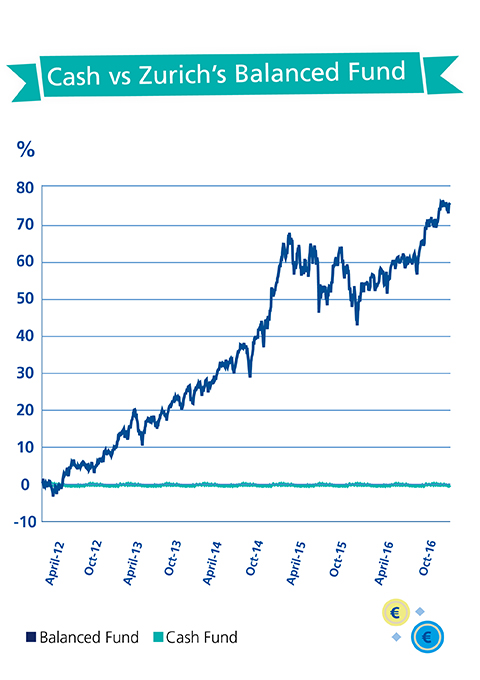

Source: Zurich Life, April 2017. Annual management charges (AMC) apply to figures quoted (30/03/12 to 04/04/17). The fund returns shown are net of the AMC deducted by Zurich Life in our unit prices. The fund returns are based on an investment in the funds and do not represent the returns achieved by individual policies linked to the funds. These fund returns may be before the full AMC is applied to a policy. The actual returns on policies linked to the specified fund will be lower because of the effects of charges and in some cases a higher management charge.

The graph above shows how one of our managed funds has outperformed cash over the past five years. It is important to be aware that investing in other asset classes, such as equities and bonds, carries the potential for higher returns than cash, but it also carries the risk of higher losses to your investment.

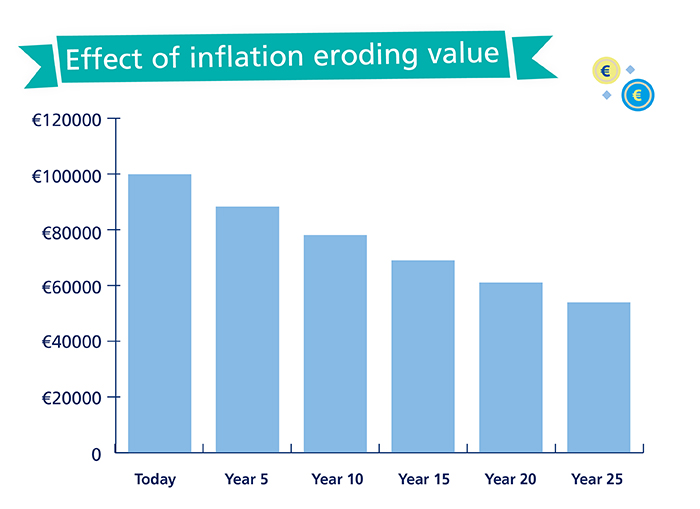

Even at an inflation rate of 2.5%, assuming no interest return for simplicity, €100,000 will be worth the equivalent of €53,939 in 25 years’ time in terms of purchasing power. A low interest rate environment means little expected return on savings held in the bank.

Source: Zurich Life, April 2017. Assumptions: Constant annual inflation of 2.5% and no interest returns for simplicity.

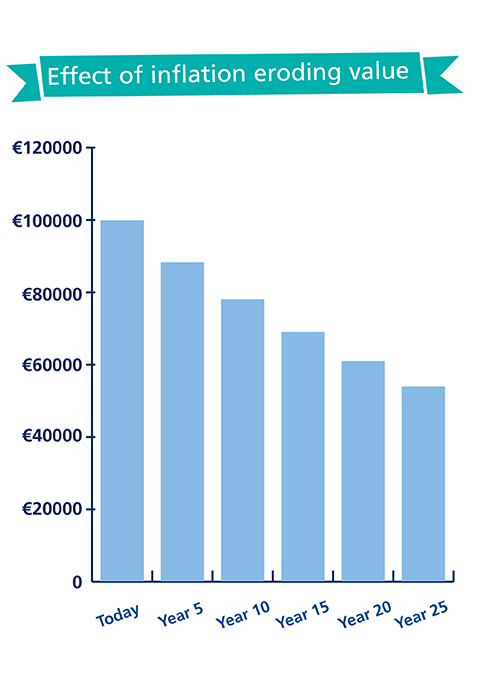

Source: Zurich Life, April 2017. Assumptions: Constant annual inflation of 2.5% and no interest returns for simplicity.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these funds you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...