February 2026 monthly investment news

Global equities advanced in January, led by emerging markets, which outperformed developed peers as a weaker dollar provided support. Read the full report on global investment markets and key fund performance.

Despite the heightened geopolitical tensions, particularly in South America and the Middle East, and ongoing debate over US policy and Federal Reserve independence, risk assets displayed moments of resilience.

Gold prices performed strongly throughout the month, though it experienced a notable decline towards the end amidst heightened volatility.

In fixed income, US bond yields (which move inversely to price) finished January higher, with the largest increases seen in shorter maturities, reflecting shifting expectations around central bank rate paths.

Equity markets lacked a decisive upward trajectory, and both bonds and currencies remained volatile as investors navigated an uncertain landscape marked by political and economic crosswinds.

Market activity

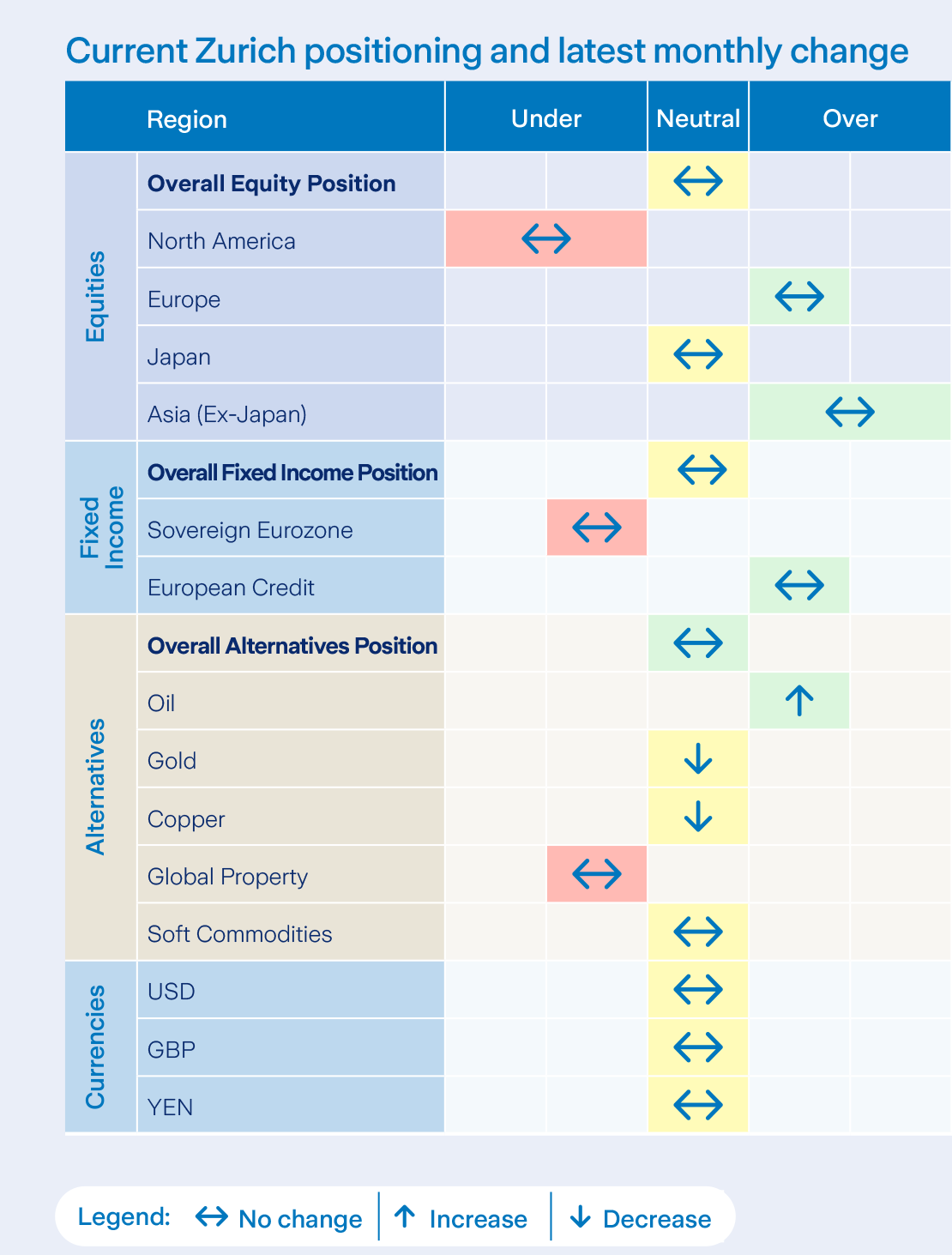

At the end of January, we reduced our allocation to Alternatives to essentially neutral in the Active Asset Allocation Fund. This was done via the sale of Gold and Copper. The proceeds were invested in oil and cash. This brought oil to modestly overweight.

This move was also reflected proportionately in the Prisma funds. Gold and many other metals had accelerated further year to date. Oil has been in the limelight to a certain extent with Iran and other tensions but much less a part of the metals’ ‘frenzy’. There were no other material changes to asset allocation in January.

Equity markets

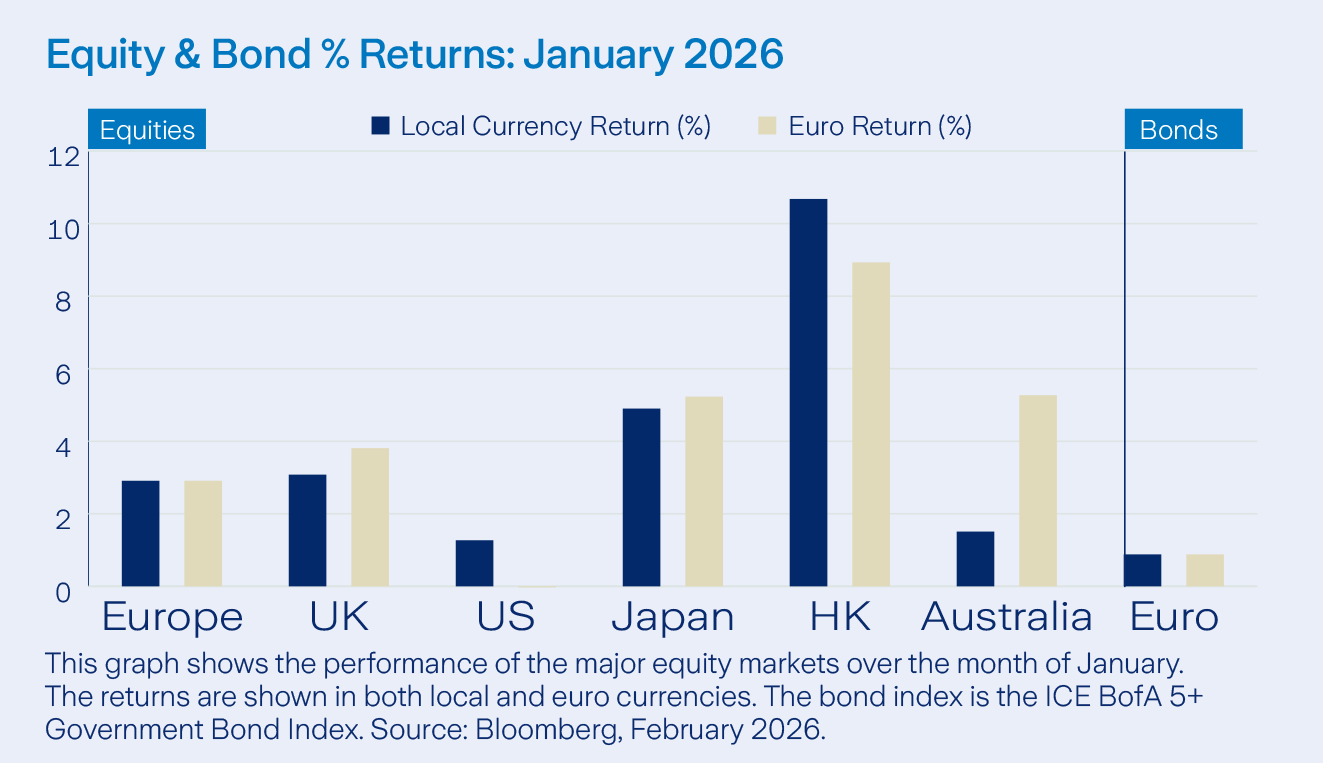

Emerging markets delivered strong returns in January, outperforming the MSCI World index. Value stocks outperformed their growth counterparts, with smaller companies also posting solid gains. Volatility increased at times, notably following renewed tariff threats from the Trump Administration.

US equities rallied late in the month, fuelled by optimism around artificial intelligence, strong tech sector earnings, and expectations of ongoing Federal Reserve easing. Geopolitical events, including President Trump’s Greenland comments, pressured eurozone equities mid-month.

In Euro terms, 8 of 11 sectors rose, led by Energy (+11.6%) and Materials (+7.9%), while Information Technology (-2.0%), Consumer Discretionary (-0.7%), and Financials (-0.5%) lagged.

Bonds and interest rates

US government bond yields rose in January, with gains focused in shorter maturities, the 10-year yield moved from 4.17% to 4.24% over the month.

The Federal Open Market Committee held rates steady at 3.5–3.75%, with Chair Jerome Powell noting balanced risks to the Fed’s dual mandate. President Trump nominated Kevin Warsh to succeed Powell as Fed Chair. Warsh is considered market-friendly, supportive of lower rates, but also advocates for reducing the Fed’s balance sheet. Meanwhile, the ECB kept policy rates unchanged and is viewed as having ended its rate-cutting cycle, with no change expected in early February.

Commodities and currencies

Geopolitical tensions, such as the US’s removal of Venezuela’s leader Maduro and threats of intervention in Iran and Greenland, created market unease. The US dollar weakened against all G10 currencies, with the euro rising from 1.175 to 1.185 USD during January.

Energy prices advanced, with natural gas benefiting from cold US weather and WTI oil ending at $65.21 per barrel. Gold saw strong gains of 13.3% in USD, as investors sought safety amid inflation and debt concerns, though a late-month sell-off followed President Trump’s nomination of Kevin Warsh as the next Federal Reserve chair, easing inflation fears.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these products you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...