Helping family members with money

Zurich’s savings policies are ideal for you to gift money to your loved ones, accumulating a fund which they can use for something they might need in the future, a deposit for a house, a holiday, or a new car. Find out more about the Small Gift Saver solution from Zurich in this article.

Zurich’s savings policies are ideal for you to gift money to your loved ones, accumulating a fund which they can use for something they might need in the future, a deposit for a house, a holiday, or a new car. Find out more about the Small Gift Saver solution from Zurich in this article.

For today’s younger generation, with rising costs and higher inflation, getting on the property ladder or buying a car can seem impossible. That’s why more and more parents, grandparents, and wider family members are doing what they can to help.

But at the back of everyone’s mind is the question – am I permitted to help family members with money, and if so, can it be done in a way that will not attract a tax liability? The short answer is yes, you can help family members, and yes, it can be done in a tax efficient manner – provided you follow certain rules.

Understanding Capital Acquisitions Tax

Capital Acquisitions Tax (CAT) is a tax you pay on gifts and inheritances. It applies to both inheritances (from someone who has passed away) and gifts (from someone still alive). CAT is only due if the value of the gift or inheritance is above a set tax-free threshold and this threshold varies depending on your relationship to the person giving you the gift or inheritance.

The current tax-free thresholds for CAT are:

| Group A: | €400,000 when the gift or inheritance is received from a parent. |

| Group B: | €40,000 when the gift or inheritance is received from another ‘blood relative’ e.g., grandparent, aunt, uncle. |

| Group C: | €20,000 when the gift or inheritance is received from anyone else. |

When a gift is passed to a recipient, the value of that gift – monetary or otherwise – will either reduce the tax-free amount or give rise to a tax liability where the value exceeds the tax-free amount. Example – what happens if I gift €50,000 to my daughter or to my niece?

| Amount gifted | Recipient of gift – daughter | Recipient of gift – niece |

| Tax-free Threshold | €400,000 |

€40,000 |

| Residual threshold after gift |

€350,000 | - €10,000 |

| Tax payable | €0 |

€3,333 (€10,000 x 33%) |

While a daughter won’t have a tax liability, the threshold has been reduced for any gifts or inheritances she may receive in the future. However, a niece will have a tax liability because there is €10,000 over the threshold, which is taxable at 33% giving a payment to Revenue of €3,333.

Take advantage of the Small Gift Exemption

The Small Gift Exemption allows a person to gift up to €3,000 a year to another person and it won’t attract a tax liability, nor will it reduce those tax-free amounts allowable on gift or inheritance tax. This means two people e.g., parents or grandparents, can gift a total of €6,000 every year to a person such as a child or grandchild.

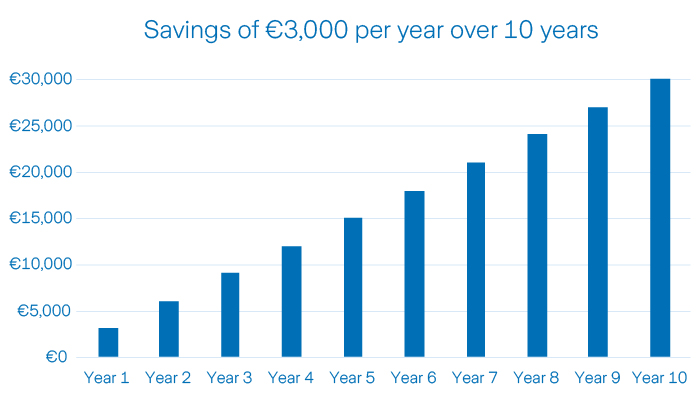

What would happen if I ‘gifted’ €3,000 to my daughter – each year?

Assuming a parent gifted €3,000 into an account, which gave no interest nor any fund growth, there would still be a considerable fund available to your daughter. And she’d have no liability to any Capital Acquisitions Tax on that fund. After 10 years, she would have €30,000 available to her for a house deposit, a new car or to fund that trip around the world.

See how your gift can grow over time

By choosing to invest your yearly gift, it’s possible for the total value to surpass the original investment. Assuming an annual growth rate, your gift of €3,000 per year over 10 years could be worth more than the total amount saved. Investing for growth helps you make the most of every contribution.

Utilising the Small Gift Exemption with Zurich

To help people take advantage of the small gift exemption in a streamlined and efficient manner, 20 years ago Zurich created the Child Savings Plan, now also known as the Small Gift Saver.

Minor Children under age 18 at outset

If the person you are saving for is a minor child under 18 years old, Zurich’s Small Gift Saver, a unique plan where the child owns the policy to which the money can be contributed by you, the payor. This is done by way of an Assignment, a transfer of ownership from the original policy owners to the minor child. Again, once the annual contribution or monthly equivalent is €3,000 per calendar year, no liability to CAT will arise.

Children over age 18 at outset

If the person you are saving for is over 18, they can take out any of Zurich’s selection of savings policies and you, as the payor, can pay the contributions into that policy. If the annual contribution is €3,000 per calendar year, no liability to CAT will arise. Zurich’s savings policies are ideal for you to gift money to your loved ones, accumulating a fund which they can use for something they might need in the future, a deposit for a house, a holiday, or a new car.

Take the next step

When it comes to your savings, Zurich is committed to doing the best we can for our customers. So, if you’d like to take the next step, get in touch today.

Talk to your Financial Broker or Advisor Call our Financial Planning Team on 0818 202 102

While this product is officially named Child Savings Plus, for the purposes of this article we refer to it as the Zurich Small Gift Saver to highlight how it helps to make the most of the small gift exemption when saving for a child’s future.

This publication has been prepared for general guidance on matters of interest only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice.

Regular Premium Assumptions: An annual management charge of 1.35% and a contribution allocation rate of 101% with no surrender penalties has been allowed for. A government insurance levy applies, currently 1% as at January 2026 and may change in the future. The contributions above are inclusive of this levy. We have assumed a gross investment return of 5.5% per annum on your savings based on an investment in Prisma 4. The return is based on an investment in the fund and does not represent the return achieved by individual policies linked to the fund. It is assumed that on death, encashment, partial encashment, assignment of a policy or on the 8th policy anniversary, tax is deducted on the gains made at the current rate of taxation (38%). These assumptions and figures quoted are for illustrative purposes only and are not an offer of contract. The information contained herein is based on Zurich Life’s understanding of current Revenue practice as at January 2026 and may change in the future.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these products you may lose some or all of the money you invest.

Warning: These figures are estimates only. They are not a reliable guide to the future performance of your investment.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...