September 2025 monthly investment news

Last month brought solid returns across major asset classes. The second-quarter earnings season continued, with Nvidia standing out for exceeding sales and earnings expectations.

At the Federal Reserve’s annual Jackson Hole meeting, Chair Jerome Powell noted a shift in economic risks, suggesting the potential for policy adjustments. President Trump dismissed the head of the Bureau of Labor Statistics, and later sought to remove Fed Governor Lisa Cook, putting central bank independence in the spotlight.

Despite these developments, markets responded calmly: long-term Treasury yields edged up, while the dollar weakened slightly. Overall, the month reflected steady market performance amid notable corporate results and ongoing discussions about monetary policy and central bank independence.

Market activity

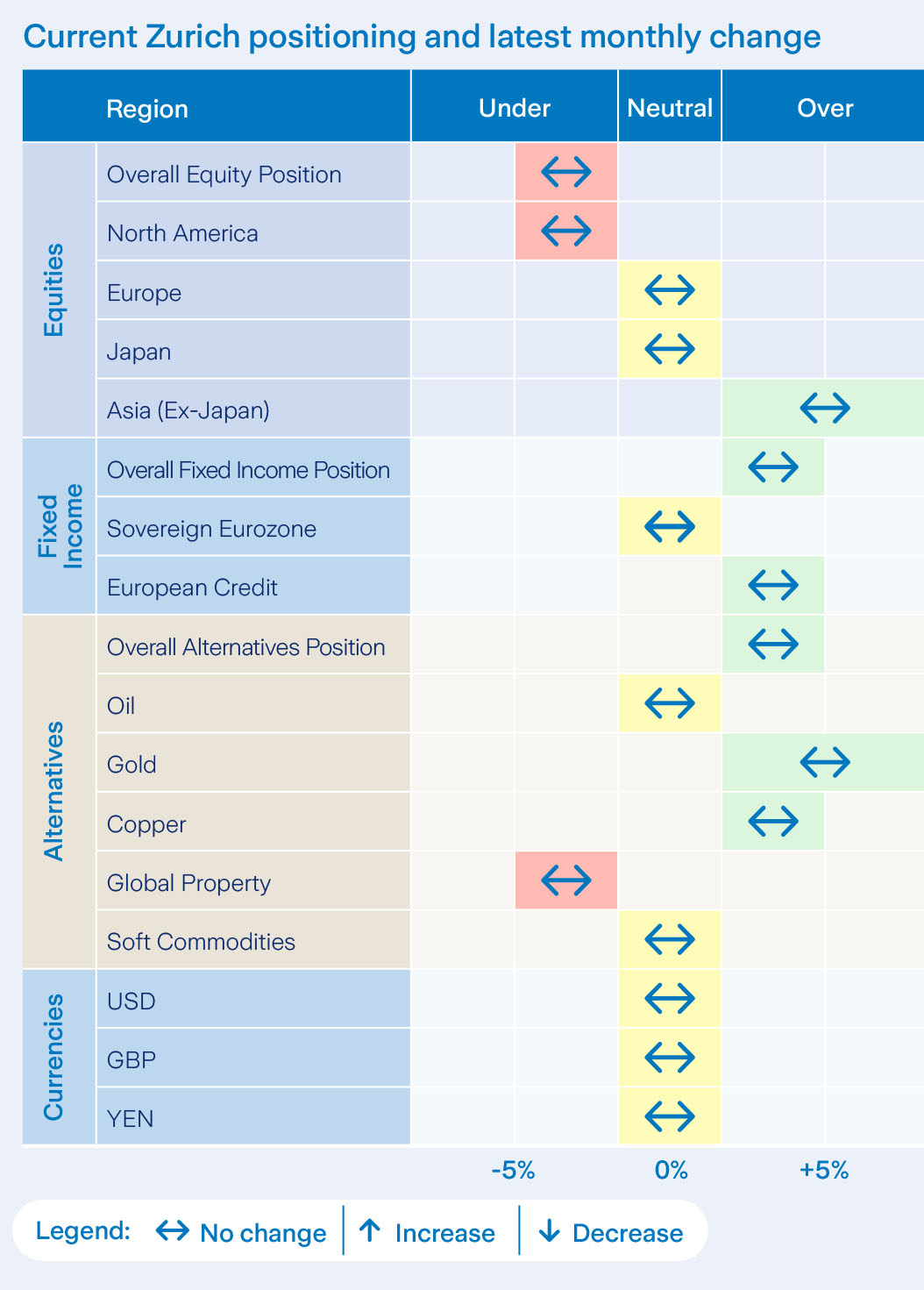

We made several active asset allocation decisions through August. We reduced our property holdings in the AAA and Prisma funds, reallocating the proceeds to cash. Later in the month, we increased our alternatives exposure in these funds by allocating more to gold, which was funded by trimming our short- and medium-term bond positions.

Within our multi-asset funds, we now maintain a modest underweight in equities in the the Active Asset Allocation fund relative to the midpoint. Regionally, we are underweight US equities, overweight Asia Pacific, and hold a neutral stance on Europe and Japan.

From a sector perspective, we favour Consumer Discretionary, IT, Materials, Financials, and Industrials, while remaining underweight in Staples, Energy, and Utilities. We also have an overweight position in gold and a slightly short bond duration.

Equity market performance

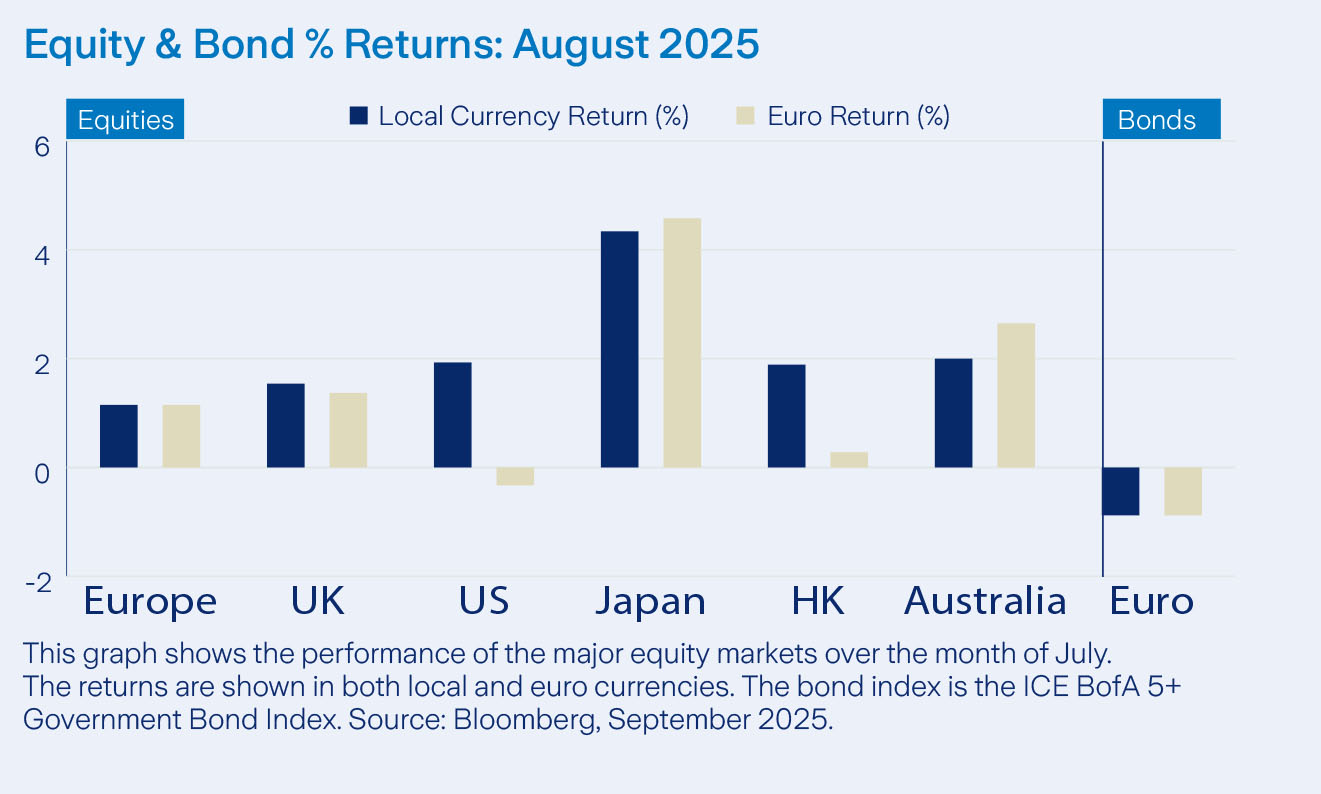

US equities reached fresh highs in August, with technology stocks remaining central as several mega-cap firms delivered strong Q2 earnings. Contrary to August’s reputation as a weaker month, eight of eleven sectors posted gains.

Materials and Health Care led with returns of 4.7% and 2.7%, respectively. Utilities lagged, declining by -2.9% in euro terms. In Europe, equities advanced, though less than global counterparts. Germany’s Q2 GDP contracted by a sharper-than-expected 0.3%, fuelling recession concerns.

In France, Prime Minister Bayrou’s call for a confidence vote on 8th September raised fresh worries over the country’s debt and political stability.

Bonds and interest rates

US Treasury yields dropped at the beginning of August, with the 10-year yield reaching as low as 4.19%. This decline followed official data showing fewer new jobs created in July and downward revisions to previous months’ figures.

In response, the US President promptly dismissed the head of the reporting office, leading markets to more seriously consider the likelihood of an imminent Fed rate cut. Political pressure from the Trump Administration intensified throughout the month. Fed Chair Jerome Powell, at Jackson Hole, signalled a growing openness to earlier rate cuts, emphasising concerns about labour market weakness over inflation.

Commodities and currencies

August was marked by volatility in gold prices, but the metal recovered late in the month, posting a 4.8% gain. A major catalyst was Federal Reserve Chair Jerome Powell’s remarks at the Jackson Hole symposium, which fuelled speculation about a possible interest rate cut in September, a development that could boost gold in the short term.

Meanwhile, global oil prices edged down, with WTI finishing at $64.01 per barrel, reflecting ongoing OPEC+ production cuts, rising non-OPEC+ output, and persistent economic challenges, including US tariffs. The US dollar weakened, as the euro climbed from 1.1415 to 1.1686 USD by month-end.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these products you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...