February 2024 monthly investment news

Following the 2023 Q4 rally, performance across asset classes was mixed in January, writes Richard Temperley.

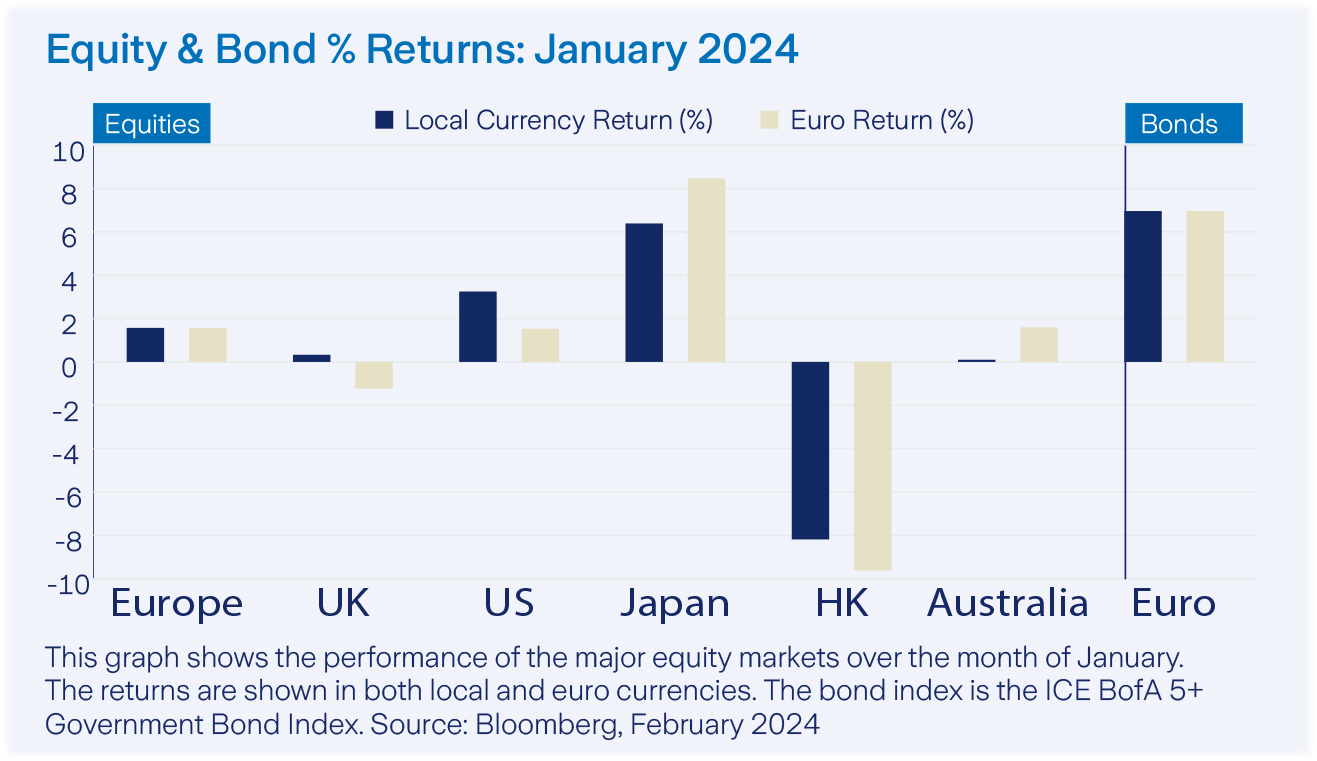

Macro data was encouraging with continued signs that inflation is taming towards a 2% target, and the labour market remained resilient. US stocks reached all-time highs in January with the S&P 500 breaking its previous highest points record.

However, equity performance cooled as the Fed pushed back against interest rate cuts in March, stating that they need to see more good data - lowering the probability of a March rate cut in the US. In fixed income markets, bond yields were off their highs but remained elevated for the month.

Activity

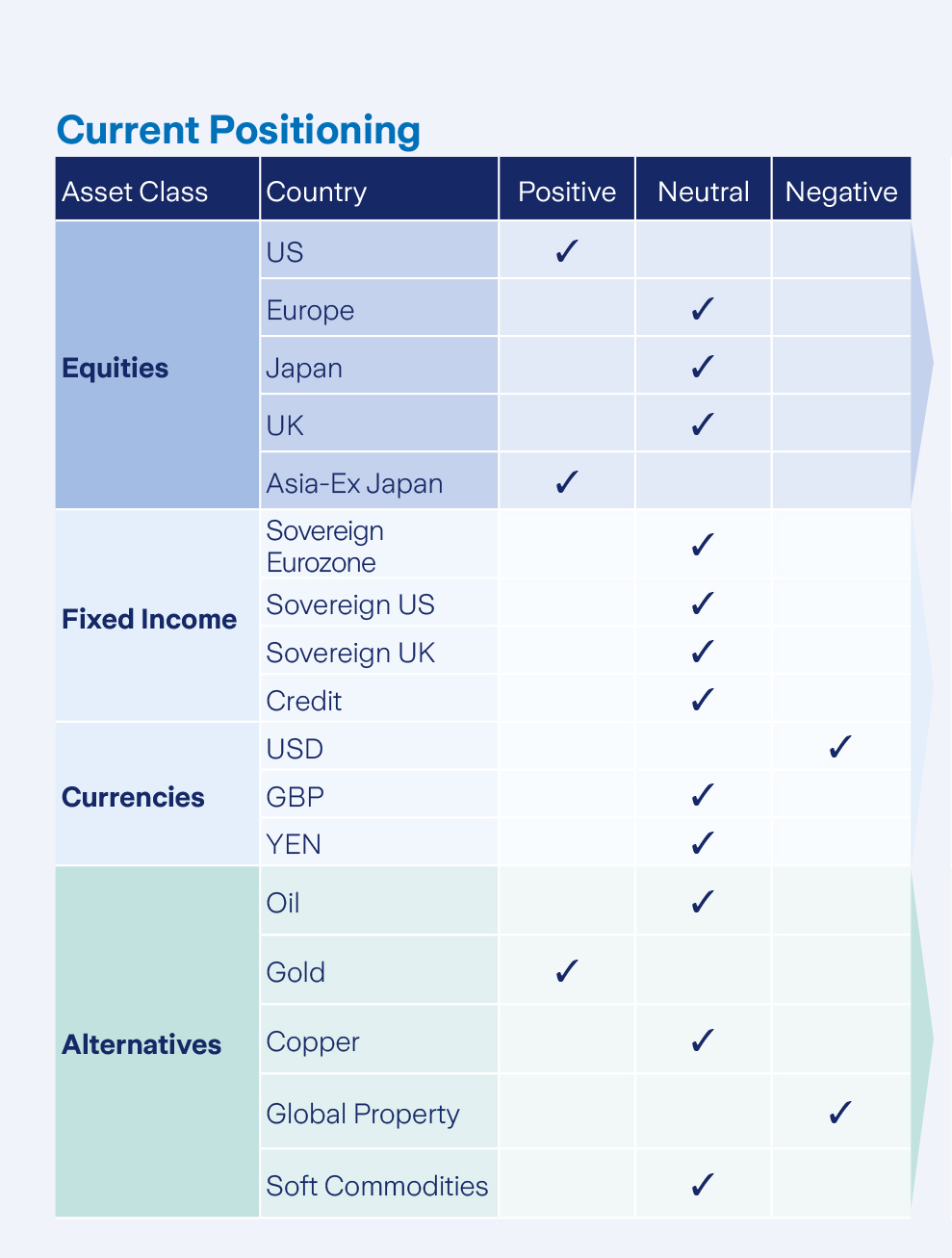

In January, we remained neutral towards equities following our steady equity reduction throughout the final quarter of 2023. We have added to short terms bonds and cash, funding this with a reduction in medium term bonds. We are slightly overweight in alternatives, namely due to our allocation to Gold.

Our EUR/USD currency hedge remains in place although it was reduced in size towards the end of 2023. Slowing inflation, moderate economic growth, resilient labour markets, moderating wage pressure, and some monetary easing is seen as a generally supportive mix for both bond and equity markets, and our current positioning allows for flexibility within either equities or fixed income, as opportunities present themselves.

Equity markets

All major equity markets were propelled higher in early January as optimism around a ‘soft landing’ scenario continued. Globally the MSCI World returned 2.91% in Euro terms for the month, with the best performing equity sector in January being Communication Services, up 6.38%.

Four of the MSCI sectors finished in negative territory with Real Estate being the poorest performing sector returning -2.83%. Several data releases including a robust jobs report pointed to the ongoing resilience of the US economy.

Following a strong start which saw record highs, the S&P 500 Index closed the month on a weaker note. The Fed pushed back on dovish market pricing for rate cuts, and explicitly noted that a March cut seems unlikely.

Bonds & interest rates

Following the positivity within the sector towards the end of 2023, bond yields steadied in January. The general consensus was that strong growth data meant that the magnitude of rate cuts priced into the markets was somewhat optimistic.

Core government bonds reversed some of last year’s gains, as markets scaled back the number of rate cuts priced for 2024. Inflation rose more than expected in January in the US, indicating the central bank has more work to do to bring down prices.

The ECB, BoE and Federal Reserve kept rates on hold at their respective January meetings and re-iterated their commitment to remain data dependent. The ICE BofA 5+ Euro Government Bond Index returned -0.87%, down significantly from its 5.71% return in December.

Commodities & currencies

Oil prices were up in January with the benchmark WTI Crude Oil reaching its highest level since October 2014. Brent Oil was also up 8.02% in January on the concern over tightening supply chains.

Tensions in Ukraine have been increasing for months after Russia massed troops near its borders, fuelling fears of supply disruption in Eastern Europe.

In the Middle East, the United Arab Emirates intercepted and destroyed two Houthi ballistic missiles targeting the Gulf country. The overarching geopolitical backdrop let to both increased prices and volatility. Copper returned 2.49% in the month. At the end of January 1 Euro purchased 1.08 USD.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: If you invest in these products you may lose some or all of the money you invest.

Warning: The value of your investment may go down as well as up.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...