March 2023 monthly investment review

February saw equities give back some of their gains from the year so far, with the US in particular faltering in the face of potentially higher interest rates, writes Richard Temperley.

Early February saw a wave of interest rate announcements from central banks with the Federal Reserve, European Central Bank and Bank of England all instituting rate rises. Notably most central banks began the month slightly more upbeat on inflation prospects however economic data released throughout February soon tempered expectations.

The release of stronger macroeconomic data has been discouraging for inflation numbers, which are still too high for the reassurance of central banks, particularly in terms of core measures which strip out volatile food and energy prices.

Although Europe continued to outperform the US, the market remains exposed to a hawkish ECB. The non-event of natural gas rationing was a positive for European economies as milder weather alleviated shortages. Stubborn inflation however means recession risk remains an area of interest.

Activity

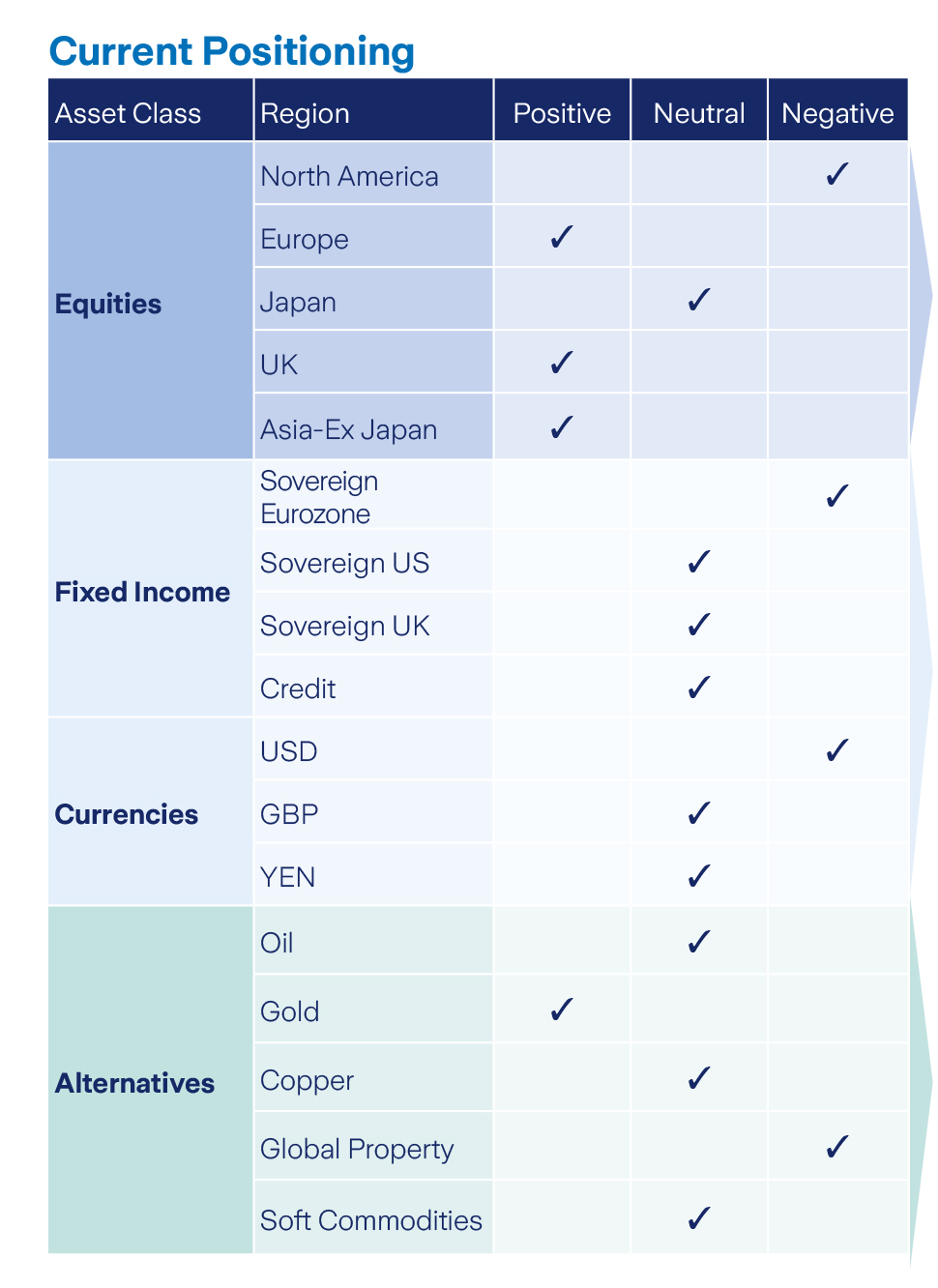

Our current position is overweight equities. During February we adjusted from neutral to underweight bonds. We also added to our equity exposure, increasing our equity content in the Active Asset Allocation fund from 48.5% to 52%, and added circa 2% across our actively managed funds.

Within equity sectors valuations remain attractive, a strong start to 2023 in equities has been driven by last years most affected sectors. Consumer discretionary for example has led the 2023 recovery and was the second worst sector in 2022.

Within fixed income, we have increased the duration of some of our eurozone sovereign bonds and reduced our allocation to corporate bonds. We are broadly neutral across our allocations to alternatives. We maintain out EUR/USD hedge which has been neutral for performance so far this year.

Equities

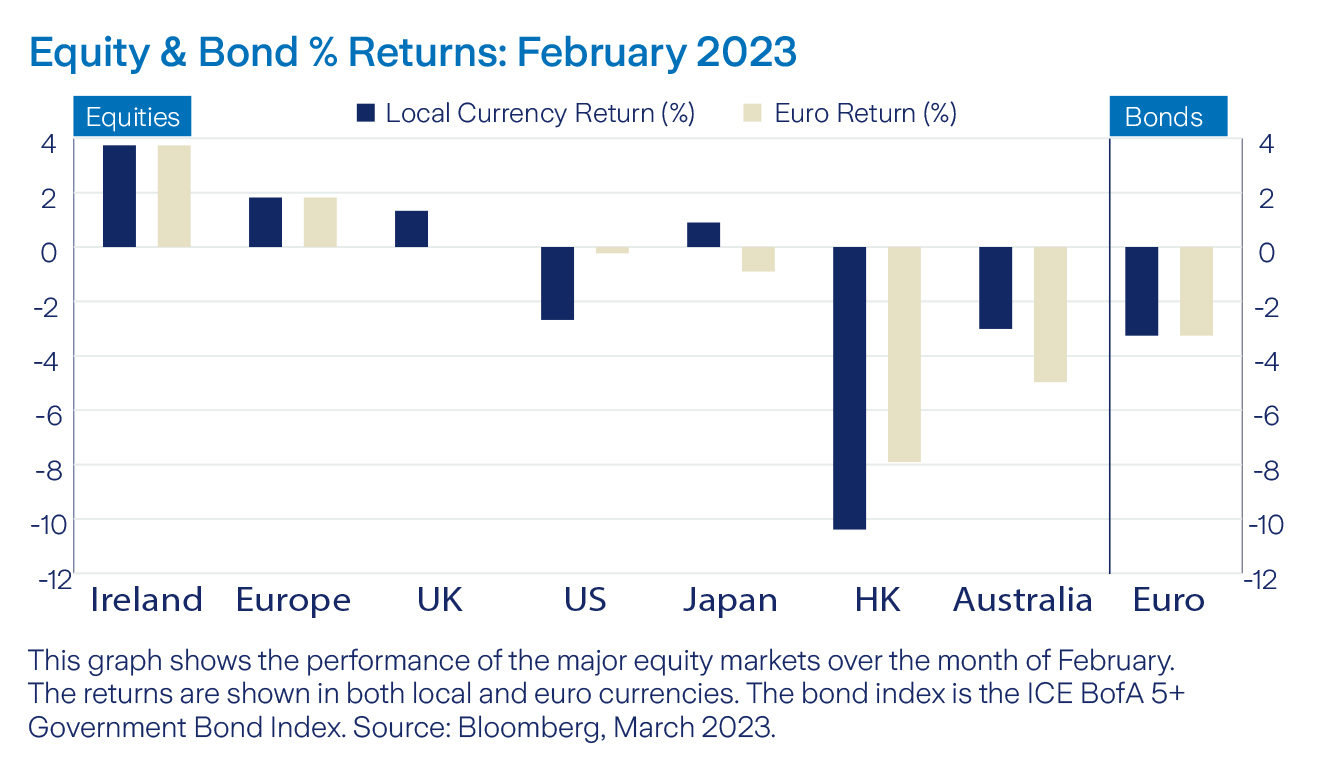

Global equities were down slightly in February losing -0.1% in euro terms after soaring in January. YTD returns are still positive as a result of previous gains, returning 5.12%. On a sectoral basis US stocks performed best in the Consumer Discretionary and Tech sectors, much of this came as companies announced layoffs and cost cutting measures which investors viewed favourably.

Euro investors in US stocks also benefitted from a strengthening Dollar, US stocks returned -2.45% in local terms and -0.1% in euro terms as losses were limited by exchange rate moves.

Eurozone equities continued their performance in February, being the only market not to post negative returns.

Hong Kong equities suffered the most as worsening US China relations and interest rate expectations caused outflows in the region. Sentiment improved towards the end of February, however the market remained down for the month

Bonds

February began with a 25-basis point rate hike (0.25%) from the Federal Reserve, a smaller increment than the previous meeting’s 50 basis points.

The yield on the benchmark 10 Year US Government Bond rose 41 basis points in February, a significant move given the recent moderation seen in sovereign bond yields. The rise in yields occurred due to higher interest rate expectations from investors who were confronted with reports of strong economic data and a tight labour market.

The strong indicators mean there could be more work for the Fed to do in terms of interest rate hiking. The higher yields resulted in a negative month for much of Fixed Income markets with the 5+ Year Euro Government Index returning -3.3% in February.

Commodities and currencies

A broad basket of commodities showed negative performance in January, with the Bloomberg Commodity index returning –2.5% in euro terms.

Year to date, copper, which is often used as a barometer for global economic health, performed better returning 8.1% in euro terms. The reopening of China’s economy has been seen by many as a major factor behind copper’s performance.

Energy prices continued to fall in February, being a large contributor to the lower overall headline figures of inflation seen globally. In currencies the US dollar strengthened slightly against a basket of peers in February on the back higher interest rate prospects in the US. At the end of February 1 euro bought 1.06 dollars.

Read the full March 2023 Monthly Investment Review here.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: If you invest in these funds you may lose some or all of the money you invest.

Warning: The value of your investment may go down as well as up.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...