May 2023 monthly investment review

April was characterised by the release of Quarter 1 earnings reports from the world’s largest companies, writes Richard Temperley.

Earnings were broadly mixed, however many companies, particularly tech firms, beat low expectations. Globally, equities saw marginal positive returns with volatility moderating significantly.

The outlook for many economies deteriorated in April as indicators suggested contraction in the likes of the US and the UK. Despite this, core inflation remained sticky, leaving a tough task for central banks.

Services PMIs in the US suggest that activity in this sector remains robust, which has contributed to stubbornly high inflation figures. On the other hand, manufacturing activity appears to have slowed, pointing to an economic slowdown.

Notably, April did see fears that were associated with the March banking turmoil subside. In addition to company earnings, focus shifted back towards monetary policy for many investors with major Central Bank interest rate decisions due in May. Slower growth prospects globally, has meant that a change in the prevailing tight monetary policy seen throughout much of 2022 is now a real possibility. For the most part however, interest rate expectations remained elevated.

Activity

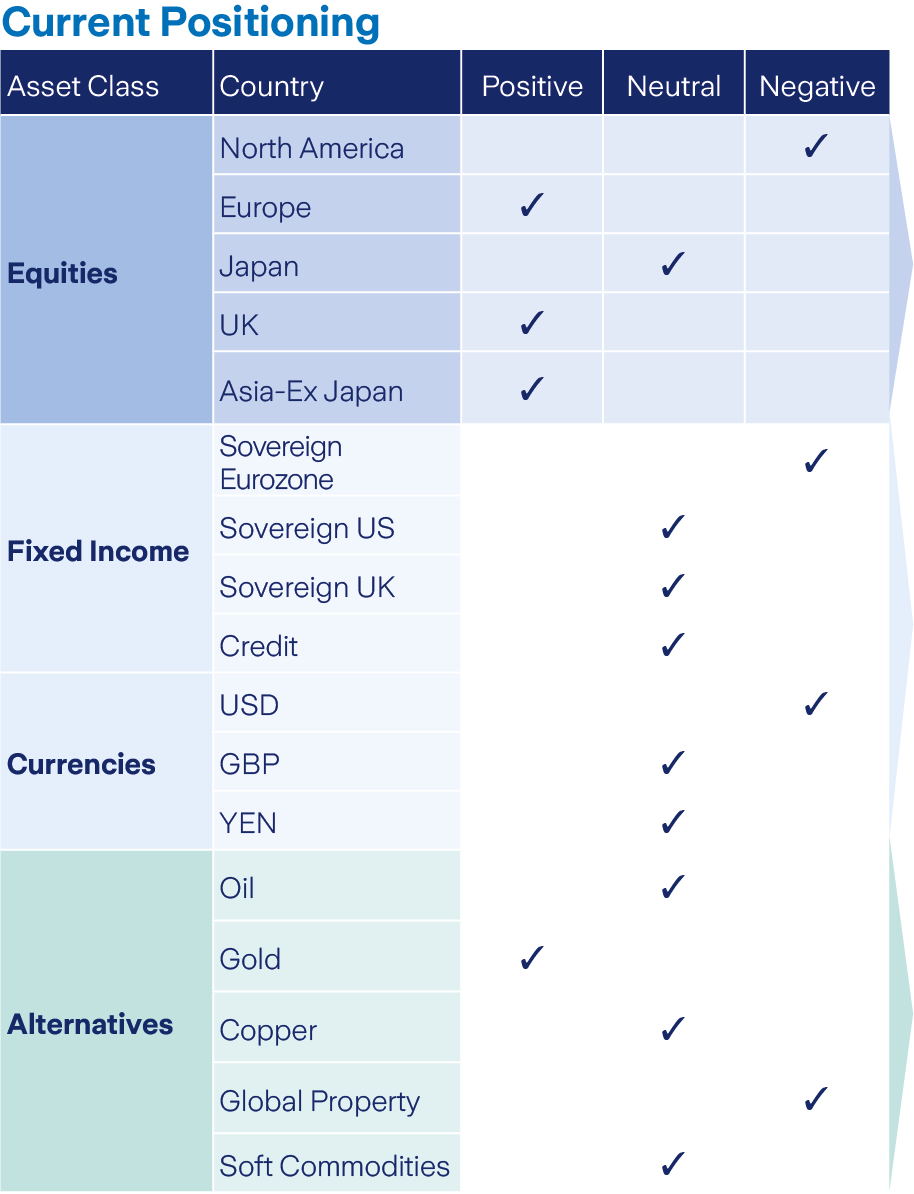

A preference for equities over other asset classes was maintained in April. Zurich have taken the opportunity to buy into dips and we have added to our equity content within multi-asset funds twice so far in 2023.

In terms of fixed income, we have an improved outlook for bonds in 2023 and have moved from negative to neutral. In this respect we have added to the duration of our fixed income holdings. On a geographical basis we hold a current preference for Eurozone, Asia Pacific ex Japan, and the UK.

Within equity sectors, we prefer information technology and consumer discretionary. Our Dollar currency hedge remains in place and has been beneficial so far this year.

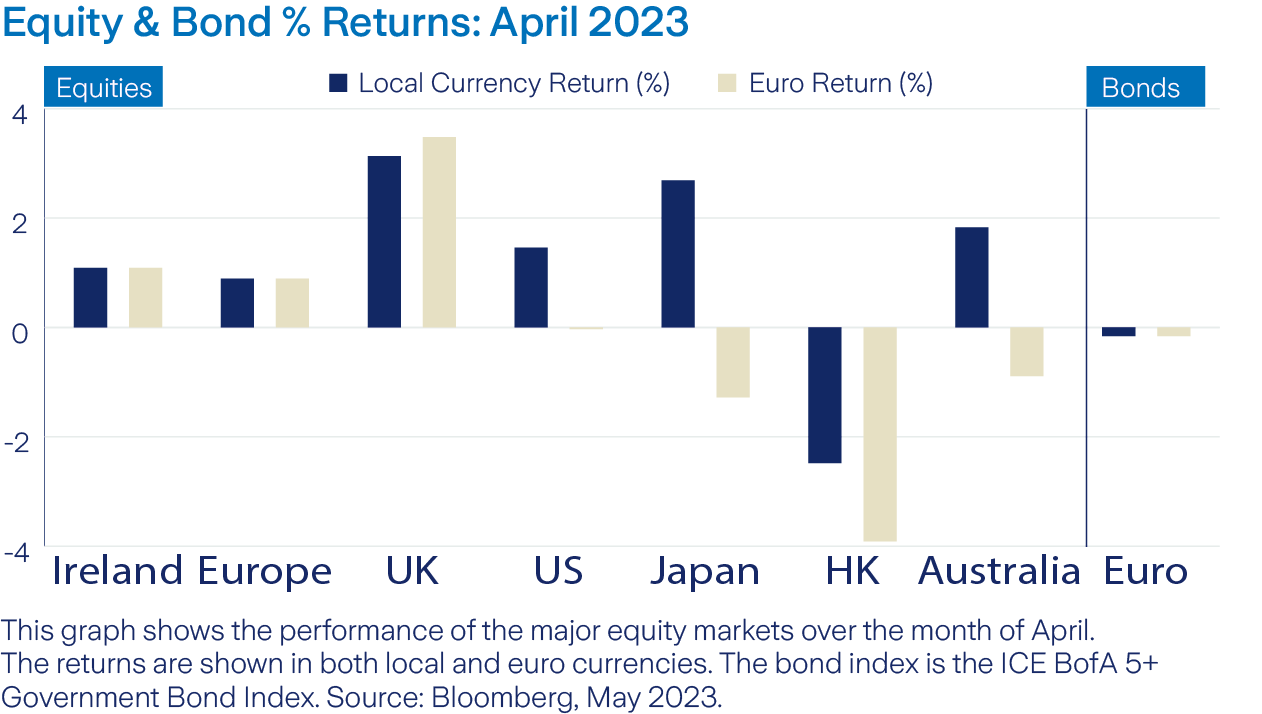

Equity markets

The UK was the best performing major market in Euro terms throughout April, returning 3.84%. This came after a poor previous month for UK equities and was largely driven by a rebound in financial sector stocks. The worst performing major market was Hong Kong, down -3.91% in euro terms. This came as the Asia Pacific region as a whole suffered a down-trend in share prices in the midst of poor US-China relations.

Foreign direct investment from US investors to China has declined over recent months, despite strong Chinese GDP growth. On a sectoral basis, financials witnessed a rebound from their March lows after sentiment improved for US banks. Globally, consumer staples were the best performing sector in April, returning 2.79% in euro terms, this came as Q1 earnings reports suggested strong profitability amongst these companies.

Bonds and interest rates

April saw global bond volatility subside somewhat as the anxiousness following March’s banking turmoil appeared to pass and yield spreads tightened. Returns in government bonds were negative however as yields rose modestly on the back of renewed interest rate expectations, with the benchmark BofA 5+ Year Euro Government bond index returning -0.16% in April.

Corporate bonds fared better however as the outlook for companies improved in April. Year to Date bonds have still performed well and the outlook has changed from previous years as these assets begin to yield a return. Much of their underperformance in April reflects sentiment about incoming monetary policy decisions in May.

Commodities and currencies

Commodity markets have had a volatile year to date and April appeared no different with crude oil in particular appearing to show wide swings in prices. The benchmark West Texas Intermediate Crude Oil finished the week down -0.11% in euro terms as energy prices experienced a slowdown.

Meanwhile copper, which is used in a wide range of manufacturing and is often seen as a barometer of global economic health, finished the month down -6.44% in euro terms as demand tapered off amid recession concerns. The euro continued to strengthen against the Dollar throughout April, albeit at a slower rate than previous months. At the end of April 1 Euro purchases 1.1019 US Dollars.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these products you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...