Markets deal with change

In his monthly review of the investment markets, Richard Temperley finds a high level of volatility but with strong returns from a number of asset classes, especially equities.

Equity markets saw a sharp correction at the beginning of the year, with the world index down 15% on the back of Chinese economic growth concerns and severe oscillation in the oil price. However, the rest of the year saw a strong, if somewhat volatile, upward trajectory with the world index rising by over 31% from its low point in mid-February.

Markets took a number of key events in their stride - Brexit, the US presidential election result, the Italian referendum result and a US interest rate rise. It was a case of all news is good news. Equities remain attractively valued on a relative basis compared to bonds and cash, although they have become more expensive on an absolute (P/E ratio) basis. Eurozone government bonds were supported in the first half of the year by monetary policy action, however they offer little long-term value and have recently come under some pressure.

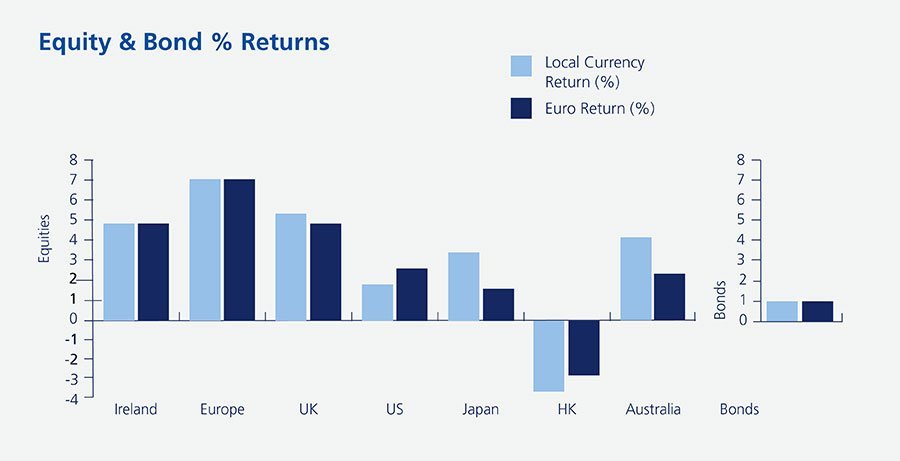

This graph shows the performance of the major equity markets over the month of December. The returns are shown in both local and euro currencies. The bond index is the Merrill Lynch over 5 Year Euro Government Bond Index. Source: Bloomberg, January 2017.

Equities rose strongly again in December as market participants continued to react positively to the US presidential election result and were unperturbed by the US rate rise mid-month. The new US administration is expected to cut corporation tax rates and to introduce an expansionary economic policy, such as increased infrastructure spending. Markets await with interest the US Q4 earnings' results season which begins in the second week of January.

World equities rose by 3.0% during December, adding to November's 4.4% move, and have given a total return of 11.9% for the full year. With the exception of Hong Kong, all of the major equity markets were up in local currency terms in December ranging from 1.8% in the US to 7.0% in Europe. For 2016 as a whole, the strongest equity markets in local currency terms were the UK (+14.4%) and US (+9.5%).

Following a number of months of sector rotation from 'bond-proxies' into economically sensitive cyclical stocks, there was a partial reversal in December due to profit-taking. In the US in December, bond-proxies such as telecoms, utilities and real estate rose by 8.1%, 4.6% and 3.8% respectively. However, cyclical stocks clearly outperformed defensive areas in the US in 2016 with energy (+23.7%) being the best performing sector; healthcare (-4.4%) the worst.

Bonds and interest rates

The Merrill Lynch Euro over Five Year Index rose by 1.0% in December, following hefty falls in October and November, giving a full year return of 4.9%. Eurozone bonds had been supported up to the end of July by economic growth concerns and increased quantitative easing. However, they are now facing an environment of higher US rates and the prospect of a reflationary US economic policy. Italy has been the big under-performer in 2016, rising by just 0.7%.

The German 10-year bond yield fell over the month from 0.28% to 0.21%. The yield had hit an all-time low of minus 0.19% on July 8th. Equivalent US rates rose again from 2.38% to 2.44% reacting to the mid-December rate rise and the likely change in US economic policy by the incoming administration.

The markets now expect at least two further US rate rises, of 0.25% each, during 2017. Eurozone rates are likely to remain at current ultra-low levels for at least two years.

Commodities and currencies

Commodity prices overall were up by 1.7% in December and were up by a strong 9.3% for the full year. The oil price was the key driver over the full year rising by close to 50% during an extremely volatile period. The oil price increased by over 10% in December, from $49 to over $54 per barrel, reacting further to the first agreed oil output cut by OPEC in eight years.

The gold price fell again in December, down 1.6% to $1,152 per troy ounce, reacting to the 'risk-on' backdrop. However, the price was up 8.6% for 2016. The euro currency weakened by just under 1% against the US dollar during the month with the EUR/USD rate moving from 1.063 to 1.052.

Activity

Equities were maintained at a strongly overweight position during December, at the expense of eurozone government bonds, based on the relative valuation argument. Some profits were taken at the end of November in financials, following a strong upward move, with the proceeds being invested into some defensive areas. These positions were maintained during December.

This Monthly Investment Review does not constitute an offer and should not be taken as a recommendation from Zurich Life. Advice should always be sought from an appropriately qualified professional.

About: Richard Temperley

Richard Temperley is Head of Investment Development at Zurich Life Ireland. The team at Zurich Investments is a long established and highly experienced team of investment managers who manage approximately €20.8bn in investments of which pension assets amount to €9.9bn. Find out more about Zurich Life's funds and investments here.

Warning: Past performance is not a reliable guide to future performance.

Warning: Benefits may be affected by changes in currency exchange rates.

Warning: The value of your investment may go down as well as up.

Warning: If you invest in these funds you may lose some or all of the money you invest.

![]()

![]()

![]()

Related articles

Filter by category

Follow us on

![]()

![]()

![]()

![]()

![]()

![]()

Sending Response, please wait ...

Sending Response, please wait ...